To survey the aerospace and defence industry is to wonder if there has really been a downturn. Top line figures compiled by PwC tell a story of businesses surging to ever-greater highs:

|

|---|

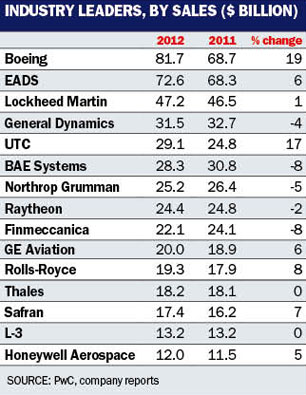

For the 100 biggest firms, 2012 was the best year ever in terms of revenue and profit, topping even 2011 - which broke the all-time record set in 2010. Last year, with surging commercial aircraft sales more than making up for a softening defence market, sales reached $695 billion and operating profit hit $59.8 billion, up by 45% and 2% respectively.

When it came to delivering commercial airliners, the 2012 total of 1,189 aircraft was a whopping 18% higher than the record year of 2011, in which the 1,000 mark was breached for the first time. To put that growth in context, go back to 1999; then, Airbus delivered 294 aircraft, half of Boeing's tally and exactly half the number it handed over to customers last year.

Considering orders, 2012 broke expectations by eclipsing the 2,000 mark for the second consecutive year and for the third time in history. With a book-to-bill ratio of 1.7:1, the industry is now sitting on a record airliner backlog of 9,000 aircraft.

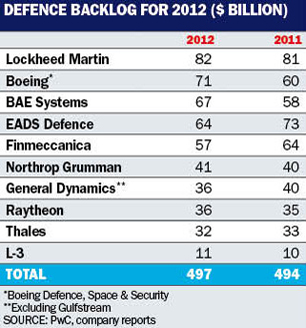

Even in the defence business - supposedly suffering from the European downturn and US sequestration - order backlogs rose, with the 10 biggest companies closing the year on $497 billion in orders to fill, up from $494 billion at end-2011.

Indeed, as PwC sums up in its 2012 industry review, a decade of steady growth in defence spending has aligned with the longest up cycle in commercial aviation history.

But, cycles cycle and what goes up does, eventually come down. Looking forward, PwC sums up: "Having well managed the growth and achieving record results, the industry must now must effectively weather the down cycle."

FLAT FORECAST

For 2013, it is no surprise to learn that PwC reckons sequestration will have a negative impact on defence industry revenue and profit.

But the "significant uncertainty" in the US defence market is clouding the broader aerospace picture. PwC reckons commercial aerospace revenue growth will slow to 4-5% - which is about the decline expected on the defence side this year. Thus, PwC estimates industry revenue to be flat in 2013.

Operating profit also looks like it will be flat, given the approximate balance of commercial growth to the defence decline. However, profits could reach new records if firms can avoid the big impairment charges that have dogged results in recent years. That may be too much to expect - declining US defence spending could lead companies to take write-offs - but PwC expects those charges to be relatively small.

|

|---|

KEY DIFFERENCES

Neil Hampson, global head of PwC's aerospace and defence practice, sees some key differences between this period, coming at the end of a decade of heavy defence spending, and the industry downturn of the early 1990s, which corresponded with US and European spending cuts at the end of the Cold War.

Perhaps echoing the chasm between the strategic clarity that characterised the years of nuclear stand-off and the relative muddle that has been the war on terror, Hampson notes that, 20 years ago, everybody in the industry knew what was happening. And, the response to that inevitable pull-back from high spending levels was industry consolidation.

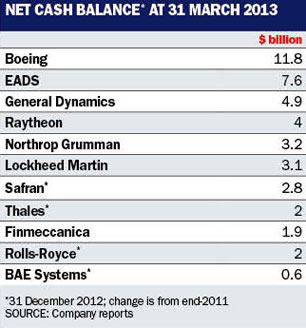

Now, however, nothing is so certain. Even US sequestration remains flexible, possibly subject to significant change following the current round of sparring between Congress and the White House. Moreover, says Hampson, the industry is in "rude health", with an "astronomical" amount of cash to hand (see table).

Consolidation would seem a likely outcome in this cash-rich industry facing revenue deterioration in the defence half of its business, which has been hugely profitable recently and historically. But that is not happening. As PwC's analysis shows, "it's not been that buoyant a year" in terms of mergers and acquisitions (M&A), notes Hampson.

Hampson likes the "phoney war" analogy for the present situation. A big downturn is expected, but has not happened. Also, the industry has a sense of having managed the 2009 downturn successfully, with no major failures. Hence, he says, there is no urgency for industry restructuring - even though companies know it has to happen eventually.

Even investment banks, usually keen on M&A from which they earn large fees, are not driving for deals. The impending downturn "is not a cliff - it's a gentle slope", says Hampson.

EUROZONE AUSTERITY

As European defence budget cuts initiated two years ago are bedded in, corporate financial prospects will stabilise. PwC sees no European budget increases until 2015, and warns that some countries may cut defence budgets further - especially for procurement - if eurozone members decide they need to tighten the austerity screws more to address their currency crisis.

However, PwC sees opportunity in Europe. As countries attempt to maintain military capability at lower cost, the traditional platform-and-equipment procurement model will be under pressure. But, the industry should be able to devise and offer more service-based capabilities.

|

|---|

PwC notes that by 2020, the UK is expected to be spending around £16 billion ($24 billion) on support services, amounting to three-quarters of the Ministry of Defence spending. PwC predicts the rest of Europe to follow that trend.

The big question, however, is whether the longstanding expectation of significant European defence industry consolidation is set to come about, finally. Some saw last year's failed attempt to merge EADS and BAE Systems as a sign of the times, but there is little evidence to support expectations of further tries to change the European defence industry any time soon.

EADS itself is giving every indication that it has no major M&A plans. It has spent down its cash pile a bit late last year and so far this year - in its push to complete the Airbus A350 programme. Its other call on cash has been, in the aftermath of the radical governance deal that has freed its shares from French and German government control, to return cash to shareholders through an ongoing share buyback. The BAE deal would have been transformational, but also out of keeping with EADS practice; nothing points to a change in the European market leader's approach to M&A.

As for other potential plays, most years feature talk of the so-called "Franco-French" deal in which Safran and Thales would join forces - but not 2013. Finmeccanica has spelled out a coherent restructuring plan which involves selling off non-aerospace businesses, but leaves little cause to expect aerospace deals other than tactical joint ventures or partnerships.

In any case, Finmeccanica would appear to have little time, or appetite, for transformational activity given the ongoing prosecutorial scrutiny of its management over allegations of wrongdoing relating to defence exports.

In a year or two, reckons Hampson, some clarity may come to the market. We may even see some companies put themselves up for sale, which would open the way, perhaps, to the restructuring that many deem inevitable.

In the meanwhile, however, do not expect any great surprises. As Hampson puts it, when all ships in a convoy are sailing in the same wind, "it's brave, or foolish, to change tack".

Subscribe to the iPad edition of Flight International, featuring more pictures and added video

Source: Flight International