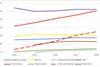

ANALYSIS: Thailand seat capacity growing at slower pace

Last year saw overall seat capacity for Thailand's key airlines expand by 5.5%, with strong international growth offsetting a decline in domestic seats.

This content is for Airline Business subscribers. Please log in or connect with our team for a personalised demo

From making its debut as a magazine in 1985 through to its evolution into an online data and analysis tool, Airline Business has forged a reputation for providing high-quality, in-depth coverage of the airline sector’s strategic and economic drivers. Our trusted insight gives users a competitive edge in the global industry.