Graham Lake, principal at Aviation Management, on why the success of efforts to tackle costs is a mixed picture across the region’s service providers

European air navigation service provider (ANSP) charges were brought into sharp relief in early June when the German ANSP, DFS, announced increases of up to 30% in 2015, leading to an immediate and predictable outcry from the Association of European Airlines.

This price jolt is a symptom of the severe difficulty that some ANSP managers face and in this case, if it happens, will place Germany at odds with its EU Single European Sky (SES) obligations.

The SES project was established with its first package of EU legislation in 2004. Two further legislative packages have since been adopted by EU member states; further refining and defining the requirements for a safer, more efficient and homogenised airspace system in Europe.

According to the EU, in 2014, 10 years from the outset of SES, in terms of cost efficiency and quality of the service provided to flights, the EU air traffic management system still stands behind its peers.

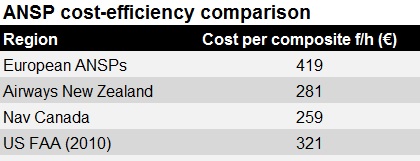

A comparison made by the Eurocontrol Performance Review Commission between Europe and New Zealand, Canada and the US FAA – all regions with similar air safety performance – shows that ANSPs in Europe are still lagging.

While European ANSPs as a group are considerably less cost-efficient than peers elsewhere, individual ANSP performance in Europe varies widely, with some delivering market-leading costs, while others still have a long way to go. The overall cost trend is downwards, in accordance with the SES performance scheme. Even so, ATM charges across the Eurocontrol area exceeded €8 billion ($11 billion) in 2013 and represent at least 6% of an airline's operating costs. For the low-cost airlines sector, the proportion can be much higher.

In Europe, typically 63% of an ANSP cost base is staff, for which costs generally increase with inflation. At the same time, ANSPs are required to reduce charges in line with SES rules, which their governments have each adopted.

Meanwhile, the hoped-for increase in ANSP revenue, expected from an increase in the number of flights, has failed to materialise, both as airlines pack more passengers into each aircraft and as average aircraft size increases. According to both Boeing and Airbus market forecasts, this trend is set to continue.

Since 2004, the transparency and reporting of ANSP performance in Europe has advanced remarkably. The Eurocontrol Performance Review Report, now published each May, shows in great detail where individual organisational ANSP progress is being made and where not.

What steps are ANSP managers able to take to improve the cost efficiency?

Pension liability is a significant consideration. Many ANSPs, since 2004, have been incorporated as wholly government owned corporations, at the same time obliged to inherit pension commitments that those same governments agreed to and which the new corporations are not equipped to support. The specifics vary by country, but these are almost always questions that can only be resolved by governments at a national level and is a part of the challenge now gaining attention in Germany.

Meanwhile there are signs that ANSPs in Europe are adopting a more commercial approach to solving their revenue and cost conundrum.

To boost revenue, some ANSP organisations are offering products and services that leverage their capabilities and services in other parts of the world, or in other markets such as defence and maritime. It is less clear that these activities are not adding more cost than revenue.

Even so, elsewhere, Nav Canada, perhaps the most efficient ANSP anywhere, has successfully built a portfolio of vertically integrated products and service to sell, developing revenue growth and cost efficiencies as a result.

It is in the area of cost reduction that real innovation is starting to take shape and to yield real progress. Cross border collaboration is delivering substantial capital and operating cost savings and harmonising cross border systems.

Ireland, along with Denmark and Sweden, established a joint Flight Data Processing System procurement programme with Thales, COOPANS, and were later joined by Austria, which achieved a reported overall 30% cost saving compared with previous programmes.

Building on the lessons learned, the Irish have since joined with Italy, Canada and Denmark in the procurement of satellite-based automatic development surveillance – broadcast (ADS-B) capability from Aereon. Most recently, the IAA has joined Norway, Denmark and Sweden in ownership and operation of an air traffic control shared training facility: Entry Point North. Each of these initiatives have served to reduce capital expenditure and operating unit costs.

Airspace efficiency is also benefiting from collaboration between members of the SES Functional Airspace Blocks, reducing flight times in parts of Europe. Real progress on cost reduction and flight efficiency in the FABs has yet to be seen across central Europe in particular.

Revenue growth for ANSPs is forecast to remain low. It is the area of cost efficiency through collaboration that offers the best prospect for the necessary unit cost savings that governments across Europe have signed up to deliver. It is likely that governments will still need to play their part in solving the pension shortfall.

Source: Airline Business