Last year proved highly profitable for most of the world's biggest aerospace companies. Despite near-stagnant revenues, the industry's largest 100 businesses significantly boosted returns, with profits soaring more than 17% in dollar terms over the previous financial year, and operating margins averaging 9.3%.

The figures are based on FlightGlobal's analysis of the annual results of 100 aerospace businesses based on turnover – which once again we have carried out with Counterpoint Market Intelligence. Companies with revenues deriving almost entirely from aerospace are ranked alongside aerospace units of larger corporations – such as General Electric, Honeywell or United Technologies.

Our latest annual Top 100 company ranking shows only modest jostling for position within a table little altered from its predecessor by merger and acquisition activity. Aerospace is a business dominated by long-term contracts and programme development, and major year-to-year fluctuations in a company's fortunes are rare.

Prepare for some changes to the order next year, however, as B/E Aerospace and, almost certainly, Zodiac make their exit after their absorption by Rockwell Collins and Safran, respectively. Both these takeovers, along with Rolls-Royce's ITP acquisition, and another at the bottom end of the top 100, came too late to affect this year's listing.

One of the major pieces of M&A activity affecting this year's figures actually happened in 2015. Lockheed Martin's $9 billion purchase of Sikorsky from United Technologies that November added more than $4 billion to the revenues of its rotary and mission systems division in 2016, and helped to push overall revenues at Lockheed up 17%.

The defence giant also managed to lift profits in the latest financial year by almost 18%. This was an achievement matched by most of the 10 biggest businesses, including United Technologies, GE Aviation and Safran – which all enjoyed double-digit profit growth – although not, notably, by Boeing and Airbus.

TOUGH TIME

In terms of profitability, the top two had a torrid 2016. Boeing's sales fell 1.6% to $94.6 billion – edging it back from its progress towards becoming the first $100 billion-revenue aerospace company – and profit dropped 5.4% to $4.9 billion, while its rival in Toulouse had a year to forget. Despite a strong orderbook and deliveries for its A320 family in particular, and a reduction in R&D costs as programmes matured, Airbus was badly hit by ongoing problems with the A400M, with the company taking a charge of around $2.6 billion in 2016 against the programme. As a result, a 3.3% revenue boost to $70.8 billion was offset by a 44% fall in profit, to $2.4 billion.

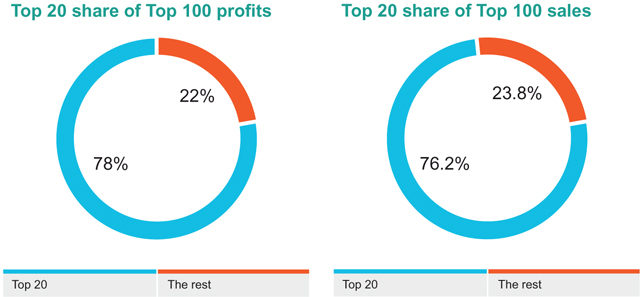

In all, while the aerospace industry follows a roughly 80/20 rule, with the biggest 20 companies having nearly 80% of overall revenues and profits, this has adjusted slightly from 2015 in favour of the smaller companies. In last year's Top 100 survey, the top 20 enjoyed 77.5% of sales and 79.5% of profits. This time, these shares have fallen to 76.2% and 78%, respectively. In fact, only two of the 20 fastest-growing companies in 2016 are among the biggest 20: Lockheed Martin and BAE Systems. On the other hand, four of the 20 most profitable companies (by operating margin) are in the top fifth of the main table: General Electric, General Dynamics, Safran and Raytheon.

This year's ranking has a familiar feel, with only one new entrant – Hutchinson, a subsidiary of French oil company Total, which makes its debut at number 83. Meanwhile, the UK's Ultra Electronics falls just outside the Top 100, mainly because we have significantly revised the aerospace sales of that company, as well as those of Indra of Spain. Elbit and Chemring have also been downgraded because we felt we were previously overstating their aerospace sales. Coming up with exact figures for industrial conglomerates that report aerospace activities across various divisions is never an exact science, of course, but we endeavour to make our estimates as precise as possible.

In some cases, companies themselves neatly segmentise their aerospace business into a division or divisions. In other instances, aerospace sales are split across various business units, in which case we have used our judgement to estimate aerospace sales. Two companies in this year's listing – Hutchinson and Nordam, a private US company that is a significant supplier of aerostructures, engine components and cabin systems – do not produce any estimates for their aerospace sales. In these cases, we have drawn on industry knowledge to come up with a figure that represents their influence in aerospace as closely as we can.

To eliminate the distorting effect of fluctuating exchange rates, we measure companies' year-on-year performance based on the currency they report in. So if a European company's revenues rise 10% in euro terms, that is how we record it, regardless of the change in the dollar exchange rate. However, the overall ranking by revenue is based on a consistent conversion to dollars. Exchange-rate fluctuations have most keenly affected sterling. The pound/dollar rate fell from 1.47 in 2015 to 1.30 after the June 2016 Brexit vote. However, what, if any effect this has had – positive or negative – on Top 100 companies that report in sterling, such as BAE Systems, Rolls-Royce and GKN, is unclear.

Aside from the Rolls-Royce, Safran and Rockwell Collins acquisitions mentioned earlier, there are no other major M&A moves in progress. Any transactions that go through between now and the end of the year would probably be too late to significantly affect next year's ranking anyway. That is not to say there have not been reports and rumours. Last year's big news was the Honeywell approach for United Technologies. In August 2017, there were suggestions of a United Technologies takeover bid for Rockwell Collins. In May, the chatter was of a Boeing swoop for Raytheon.

M&A SLOWS

In Europe, other than Safran and Zodiac, the second wave of consolidation that some expected after the flurry of activity that created EADS (now Airbus), BAE Systems and Thales at the turn of the century has not materialised. Italy's sprawling industrial champion, Finmeccanica, rebranded as Leonardo last year, and, although not without its troubles, appears a slimmer, more focused entity. Last year, Airbus finally unloaded its remaining 23.6% stake in Dassault, a legacy of 1990s, pre-EADS government influence in the defence industry. Until 2014, Airbus had held 46% of shares in the manufacturer of Rafale fighters and Falcon business jets.

The absorption by Safran and Rockwell Collins, respectively, of cabin systems suppliers Zodiac – ranked 23 with a turnover of $5.54 billion – and B/E Aerospace – 36th in this year's ranking, with $2.93 billion sales – together with the merger of US aerostructures supplier LSI and Belgium's Sonaca, will guarantee at least three new names in next year's Top 100. The LSI/Sonaca marriage brings together two companies with a combined turnover in 2016 of around $730 million. Whether the listing will change much beyond that will depend on whether there is any further significant M&A action in the coming months.

For years, there has been talk – encouraged by some of the primes – about a need for rationalisation among first- and second-tier aerostructures companies. While we have seen some smaller companies being snapped up by larger entities, it remains to be seen whether consolidation will take place further up the supply chain. In terms of financial performance generally, the theme of 2017 appears to be steady as she goes. Although there has been some erosion of commercial aircraft backlogs as orders have dropped from their peak of a few years ago, defence sales have been stable, with only makers of large business jets feeling major pain.

Source: Flight International