International air travel is about to change dramatically. Deregulation, new business models and evolving consumer behaviour - all factors that contributed to the low-cost carrier revolution in short-haul flying - will soon be playing out in the long-haul environment. At the same time, further pressure for change will come from the introduction of new aircraft technologies, the emergence of new blocks of demand from developing regions, and the increasing financial pressure on traditional flag carriers to reduce their own internal cross-subsidies between long- and short-haul networks.

Together, these developments could lead to a fundamental rearrangement of international traffic flows - or the way that the industry organises its schedules and seats to get passengers from point A to point B (often through point C). There are two key developments in long-haul traffic flows:

■ Point-to-point flying will grow, as more passengers fly direct routes rather than through hubs.

■ Remaining hubbing traffic flows could splinter, with hubbing passengers and carriers increasingly turning away from flying on ultra-thick trunk routes through airport "megahubs".

Airline markets naturally evolve toward point-to-point flying over time. In their early stages, hub-and-spoke flying predominates because very few routes have enough demand to warrant direct flying. As a market develops, however, more-travelled routes reach certain thresholds of demand, which justify direct daily services. In most cases, the overall impact is a declining share of hub-and-spoke flying.

This is especially true for international air travel. For example, a bottom-up analysis of demand prospects for the more than 10,000 city pairs between Europe and North America shows that only a third of demand reaches the threshold for direct flying today, but 39% of demand will reach that threshold in 2015 and 43% by 2025. Similar trajectories exist for Europe-Asia and North America-Asia city pairs (see chart 1).

New aircraft technology is a second factor contributing to the increase of point-to-point flying on long-haul routes. Although it is difficult to fully assess technology that is yet to be flown commercially, our analysis of the likely economics of the ultra-large Airbus A380 versus the smaller Boeing 787 and A350 suggests that the latter will have a much greater impact on the relative economics of hub versus direct flying than the former. Whereas the A380 is a continuation of a long-standing historical trade-off between aircraft size and unit cost, the 787/A350 technology represents a move to a new technology curve.

Indeed, some of the more bullish forecasts for 787/A350 technology (which for the 787 includes a reliance on assuming nine-abreast seating) would see it matching the A380's unit costs with an aircraft one-third the size. If this were to happen, we estimate an additional 10% of hubbing traffic could move to point-to-point flying.

Although we believe that hub-and-spoke flying will become less common over time, our projections show that, in absolute terms, it will remain the predominant form of traffic over the foreseeable future.

Splintering hubs

So can large airports and hub airlines breathe easy? The answer is no. We believe that whereas traffic flows evolve slowly but steadily towards point-to-point flying, a subtle yet far more disruptive change may also occur in the pattern of hub-and-spoke traffic flows. Over the past decades long-haul hubbing traffic has consolidated into ultra-thick trunk routes between giant megahubs. But it is possible that in the future this consolidation may reverse direction, with hubbing traffic splintering or unravelling across more trunk routes and more hubbing airports, as the ties that currently bind hub traffic flows to certain routes and hubs loosen.

To see what might drive this change, it is necessary to return to the discussion about aircraft technology. As airlines become more indifferent to the costs of flying a large or a small aircraft, a key plank in the logic for consolidating hubbing traffic into ultra-thick routes and megahubs potentially falls by the wayside. In a bid to offer greater frequency and/or shorter flying times, airlines would in fact have a greater incentive to use smaller aircraft and disperse their hub flying across a number of routes and airports, rather than consolidating in a limited number of trunk routes flying out of megahubs.

Other factors may also contribute to the loosening of ties between hubbing traffic and particular routes and airports:

■ New point-to-point routes: The natural evolution of markets towards a higher proportion of point-to-point flying, as discussed, will see more city pairs warranting direct daily point-to-point flying. In turn, this will give airlines a greater number of trunk routes to piggyback their hubbing traffic on, which means hubbing flows are likely to become more dispersed across routes and thus airports.

■ Increasingly open skies: Although making projections of the timetable and pattern of deregulation is difficult, if and when the next tranche of deregulation occurs, the breaking apart of traffic flows would receive a significant boost. Airlines will increasingly be able to fly schedules and seats on the basis of pure economics, in contrast to the somewhat artificial constraints imposed by today's air-rights regimes. And if increasingly open skies lead to a decline in the importance of airline alliances (because airlines will be able to reap the benefits of scale and consolidation directly through mergers and acquisitions), we will see carriers less inclined to deliver all their feed to one large alliance partner's home hub. Instead, airlines may bypass their alliance partners, and/or build codeshare relationships with low-cost carriers in other ports.

■ Reduction in internal cross subsidies: The low-cost carrier revolution in short-haul flying has exposed the extent of cross-subsidisation of transfer passengers within traditional flag carrier networks. For example, Boston Consulting estimates show that in 2005 the cost of such subsidies amounted to more than twice European network carriers' total reported long-haul profits. As network carriers come under increasing financial pressure to remove - or at least temper - these subsidies, hubbing passengers will be less likely to be lured to major network carriers and their hubs through artificially cheap connecting tickets. Aided by distribution technology, they will increasingly manage their own connections, flying more on short-haul point-to-point carriers to meet or leave their long-haul flight. Again, hubbing traffic becomes more and more up for grabs.

Hubbing potential

Putting these factors together, the potential for hubbing traffic to become increasingly splintered over future years becomes clear. To quantify the magnitude of such a trend - and to identify who might win and who might lose - we conducted bottom-up modelling of the demand outlook and alternative routing distances for all northern hemisphere long-haul city pairs.

Chart 2 shows our modelled comparison of "warranted" 2015 long-haul traffic of each major airport with its estimated long-haul volume today. Las Vegas, Berlin, Brisbane and Dublin, for example, all stand out as cities that have outstanding potential for further growth in a splintered world. On the flip side, some large hubs, such as Atlanta, Paris and Singapore, appear to have maxed out their growth potential.

The implications of these trends and developments for airlines are crucial. First, flag carriers from smaller countries will find that the trend towards more point-to-point flying promises a brighter future than they may have assumed. The advent of the new generation of mid-sized widebodies will lower the threshold at which these carriers can economically participate on routes. And for routes on which they already participate, it will improve their economics relative to larger hub carriers. Moreover, these carriers can use their broader point-to-point coverage to compete (economically) for the up-for-grabs hub traffic.

Second, for larger hub carriers, the increasing proportion of point-to-point demand will have significant implications for both their "natural" share of long-haul traffic flows and the way they structure and configure their own networks. Airlines that have ordered ultra-large aircraft will need to carefully think through their fleet deployment and scheduling strategies, as the basis for advantage upon which the fleet orders were made may change in the future. Ultra-large aircraft should be deployed primarily on routes whose point-to-point demand (rather than accumulated current hub traffic) is thickest on routes where slot constraints are highest or on routes where there is a comparative lack of alternative hub options. All large hub carriers should also think through the ways that they could use new widebody jets - for instance, to boost frequencies on important business routes or to optimise their flow of current hub traffic.

Finally, all carriers need to be aware of the change in competitive dynamics that the advent of new technology and traffic patterns may bring. Potential new entrants may find a greater resolve to chance their luck as the 787 and A350 lower the number of passengers required for breakeven flights and removes the "small-aircraft" cost penalty that has typically penalised and discouraged small-niche point-to-point players.

The implications for airports are just as crucial. Those that currently serve as significant hubs for long-haul airlines have a lot to lose if they don't take steps to understand their current position and shore it up. And nearly all airports have the potential to win new tranches of long-haul demand.

To assess the airport's underlying competitive potential managers need to consider two key dimensions. The first is geographical position - the airport's location in relation to the origin or destination cities to which hubbing passengers are travelling. The second dimension is catchment demand - the composition of demand in the natural catchment area.

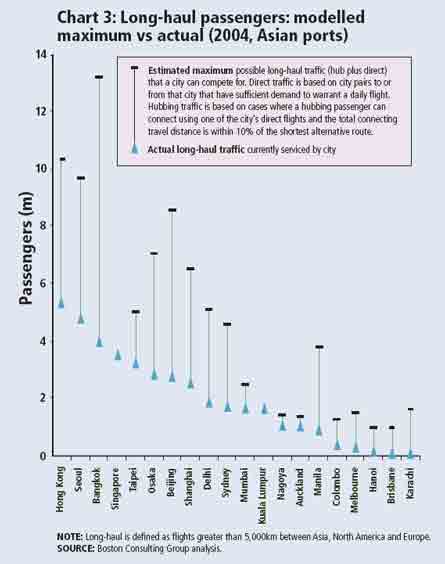

Chart 3 shows an assessment of major Asian airports along these two dimensions. It compares the long-haul capacity currently offered from each airport with the maximum amount of current traffic the airport could win on the basis of catchment demand and geographical position. We allowed a 10% leeway in calculating geographical advantage and penalised airports whose demand was overly fragmented. The outcome shows that, on the basis of current demand patterns, the airport cities with the largest gap between their potential traffic and current traffic flows are Bangkok, Beijing and Manila. Singapore and Kuala Lumpur are the airport cities with the smallest gap.

Once a manager has assessed an airport's underlying competitive potential for long-haul traffic, the second step is to consider how to compete for traffic. Here, airport managers have to become accustomed to a changing set of bases for competition. For instance, the strength of the home carrier - the primary drawing card for airports in the past - may start to decline over time.

Similarly, as airports and passengers come to rely less and less on strong home network carriers to provide short-haul and long-haul connectivity, airports will find themselves having to take a more proactive "orchestrator" role in providing the type of smooth connectivity that wins traffic flows. This will involve a number of elements, ranging from attracting the right mix of short-haul connecting low-cost airlines, to providing seamless on-ground transfers. It might even entail taking an active role in co-ordinating various airline schedules to maximise connectivity. The advent of an airport as a "virtual network provider" may not be far off.

Long-haul international travel is entering a decade of potentially radical transformation. Airline and airport managers need to assess whether they have a full understanding of these changes, and their impact on the business environment. These are complex issues. But by asking the right questions now, they will give their organisations the best chance of negotiating a path to sustainable competitive advantage in what is likely to be a very fluid world. ■

Source: Airline Business