The operating lease is a key part of the commercial aircraft industry – accounting for nearly 42% of today’s commercial jet fleet. After seeing continuous growth since the late 1970s, the operating lease fleet share has stagnated since 2008. However, that period of apparent stabilisation witnessed the rise of a new player, one that is making a big impact in the industry: the Chinese operating lessor.

The mainland Chinese operating-lessor fleet has grown from a mere 30 aircraft at the start of 2008 to over 780 aircraft today, representing 9% of the global lessor jet fleet. Including lessors in Hong Kong and Bank of China subsidiary BOC Aviation based in Singapore, the Greater China share rises to 13.5%. The mainland lessor fleet has grown at a staggering compound annual growth rate of 38% since 2010, although lessors are still very much focused on China, with two-thirds of their fleets on lease to Chinese operators. The growth story is a successful one, but it is only the beginning – what challenges and risks lie ahead?

Flightglobal’s Fleets Analyzer database shows 15 Chinese mainland-based operating lessors with in-service fleets, but that number is growing as other platforms come online. The mainland Chinese lessors can be divided into three categories: domestic domiciled, Chinese money invested offshore and Chinese airlines. The domestic-domiciled lessors base their operations in China and they include mainly the leasing arms of the major Chinese banks, but also the insurance companies (Ping An Leasing) and manufacturers (AVIC). Many also hold finance leases in addition to operating leases.

The second category involves Chinese money invested into leasing companies abroad. The first big example of this was Hong Kong tycoon Li Ka-shing’s investment in 2014 into Accipiter, a new leasing platform currently operating out of Dublin. Although this case did not involve mainland money, the endorsement of the operating leasing business model by one of Asia’s wealthiest and most respected investors sent a strong message to the Chinese community. This was followed by Bohai’s acquisition of Dublin-based Avolon, perhaps the first, rather than last move in this direction.

Finally, Chinese airlines are also participating in creating new leasing companies. Motivated by tax and financing reasons, they lease aircraft to their own airlines using both finance and operating leases. Although these lessors do not match the traditional lessor mould, they may also decide to set up a more global leasing platform as other airlines have done recently (ie, Lion Air and Transportation Partners).

Challenges and risks

Chinese lessors have grown at a tremendous pace, but as their fleets age and the economic conditions evolve, they will begin to face particular challenges and risks.

Firstly, being based in China poses particular challenges to the global lessor. One of the more efficient locations to base a leasing company is Dublin because it offers the lessor special advantages:

• Tax treaties that affect withholding taxes and depreciation policies, both of which have very important implications on a lessor’s cashflow

• Strong legal structure

• Availability of talent and expertise

• Availability of financing sources and financial markets

China is not short on capital for the leasing business as most lessors are subsidiaries of state-owned banks with mandates to invest in leasing. However, China still has a way to go to achieve a world-class lessor system, although progress is being made through the development of free trade zones and human capital.

Chinese lessors have been focused on adding aircraft to their portfolios, so they have mostly only operated at the early stages of the leasing life cycle. As a crucial final step, lessors have to actualise an acceptable residual value at the end of a lease for them to “cash in” on their investment and achieve their target rate of return. The Chinese lessors’ ability to re-market aircraft is still largely untested.

The bulk of the Chinese lessor growth has occurred in the past six years, characterised by recovery of the global economy, a boom in the aviation industry with record aircraft orders and airline profits, and strong economic results in China. By contrast, established foreign lessors have had to weather the effects of 9/11 and the global financial crisis.

With economic fluctuations, airline bankruptcies follow and lessors are often forced to repossess aircraft from bankrupt lessees. Since 2000 there have been more than 1,100 instances of leased aircraft with a bankrupt lessee. The handling of a repossession and re-marketing event is crucial to the lessor’s bottom line and each of these events represents a valuable learning experience. Chinese lessors have had virtually no experience with lessee bankruptcy. The first real test came late last year after two Chinese-owned Transaero Airbus A321 were grounded when the carrier ceased operations.

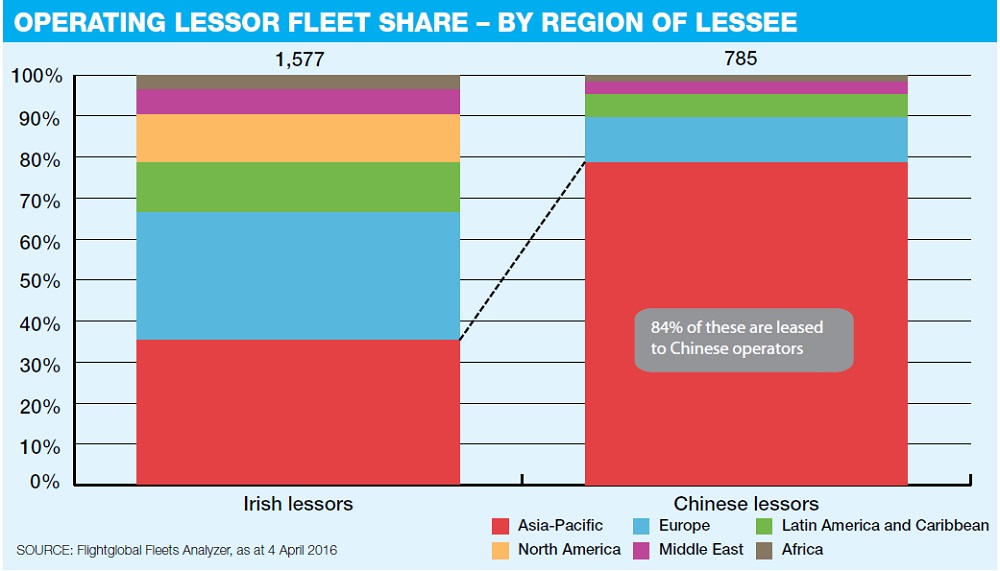

Diversification

The leased fleet of Ireland-based lessors is spread all over the world, with the highest concentration in Asia-Pacific at 35%. In contrast, Chinese lessors have 80% of their fleet within Asia-Pacific, 84% of which is leased in China. Chinese lessors surely have an advantage navigating the domestic market compared to foreign lessors. Also, if Chinese airlines continue to demand yuan financing, then Chinese lessors would be best placed to provide that (if they are willing to take the currency risk). However, the Chinese lessor fleet lacks geographic diversity and is therefore vulnerable to the economic volatility of one country.

The focus on China also makes for a very competitive market, with so many Chinese lessors all trying to fight for a piece of the same pie.

One further challenge comes when it is time to remarket the aircraft. Lessors use their global networks to remarket to airlines around the world, but a lessor that has few lessees outside of China and limited global experience will be hard-pressed to find a buyer for aircraft that come off lease. Remarketing within China so far does not seem like a viable option as Chinese carriers prefer new metal.

The Chinese lessors have grown quickly to become formidable players on the global leasing stage. However, as lease returns become due and economic conditions change, the Chinese lessors will have to deal with the challenges of operating as a global lessor based in China, conducting business during a downturn, re-marketing aircraft and achieving portfolio diversity.

Thomas Kaplan is senior analyst with Flightglobal's Ascend team in Hong Kong

Source: Cirium Dashboard