Once thought of as short-term irritants, Chinese aircraft lessors have grown to a size where they are changing the dynamics of the traditionally Western-dominated industry.

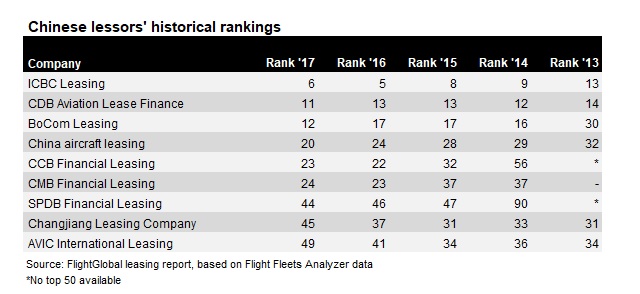

FlightGlobal’s latest lessor ranking report demonstrates just how large Chinese lessors’ fleets have grown: between 2016 and 2017, the value of the fleet managed by Chinese lessors grew 15%. This indicates that they continue to take market share from Western players that have traditionally been the major providers of capital to the industry.

Since Beijing allowed banks to start their own leasing units in 2007, a number of operating lessors cut their teeth providing capital – mostly through sale-and-leasebacks – to meet the strong demand from domestic airlines. Over time, operating leasing has become a key source of aircraft for Chinese carriers, with a November 2017 analysis by Fitch Ratings estimating that over 40% of deliveries that year were lessor-owned.

But China's lessors are not just expanding at home. Thanks to deep pools of capital, a number of lessors have established their place in the international market usually by starting branches in Ireland.

ICBC Leasing has been among the most aggressive, and is now firmly inside the ranks of the top ten global lessors. While it has made a number of acquisitions through the favoured sale-and-leaseback market, it has also placed speculative orders with Airbus, Boeing and Comac, and acquired aircraft from other lessors. Earlier this year, it engaged former GECAS boss Norman Liu as a special advisor, signaling its intent to grow further globally.

CDB Leasing, meanwhile, has carved out its aircraft leasing activities into Dublin-based CDB Aviation Lease Finance. Under the leadership of chief executive Peter Chang, an alumnus of Guinness Peat Aviation, it too has placed major forward orders for Airbus A320s, Boeing 737s and 787s.

Other Chinese lessors to have hurtled up FlightGlobal’s rankings include BoComm Leasing, China Aircraft Leasing and CMB Financial Leasing.

Interestingly, over that same period, AVIC International Leasing has fallen a few ranks. While it may have the heft of a state-owned aircraft manufacturer behind it, the lessor appears to not have kept up with the breakneck pace of growth of the bank-owned lessors.

At the same time that Chinese-headquartered lessors have grown organically, so too have those acquired by Chinese companies and located elsewhere, such as BOC Aviation and Avolon. Despite the latter facing some issues as ultimate parent HNA Group continues its restructure, its strong orderbook and acquisition last year of CIT Aerospace place it firmly in third place on the chart.

Although there are fewer merger and acquisition opportunities in the market, Ping An, ICBC and AVIC are reportedly among those looking at targets including Sky Leasing and Nordic Aviation Capital.

EXPANSION MODE

From a virtual standing start a decade ago, China’s lessors have rapidly caught up with their western counterparts. Some say they have cut aggressive deals to build up their portfolios, which has led to highly competitive sale-and-leaseback deals being cut, and some downward pressure on lease rates.

Fitch says that these lessors' focus on expansion means that they may “price risk differently from established players”.

“Leasing subsidiaries of leading Chinese banks also benefitting from their parents' funding and capital support, which may lower their funding costs and provide an advantage over standalone global competitors,” it adds.

But there are signs that more Chinese lessors are expanding from their traditional focus on sale-and-leasebacks of new aircraft to focus more on full-cycle leasing. That is in part driven by the first sale-and-leaseback deals done by the oldest lessors coming to the end of their lease terms. A number of those lessors have admitted in recent years that this will mean they have to gain new skills in transitioning aircraft to other operators, or potentially managing them out to end-of-life.

That pressure has lessened somewhat in the short-term. Some lessors have reported that Chinese carriers, which have favoured churning aircraft at the end of their leases, are now extending them to keep up with the strong passenger demand in the country.

Other lessors are also taking their first steps in transitioning aircraft out of the country and to the global market. For example, China Aircraft Leasing recently completed the transition of a 21 year old A321 from Sichuan Airlines to a new lease with Danish Air Transport.

HERE TO STAY

With Chinese lessors now playing such a key role in the market, there is no doubt that they are here to stay. For some, the question now is how much their presence in will reshape the dynamics of the global market.

While not referring directly to any particular companies, BOC Aviation chief executive Robert Martin said at the ISTAT Asia event in May that some new aircraft operating lessors were acting in ways that reflected their heritage as finance lessors.

"Finance lessors don't take maintenance returns. Finance lessors don't worry about return conditions and whether it's full-life or half-life at the end of the lease as much as traditional operating lessors," says Martin.

He suggested that the heritage of those financial-cum-operating lessors was starting to impact the market dynamics of the operating leasing world.

Other observers have also said that Chinese lessors have made “aggressive residual assumptions” in some of the deals that have been written, particularly on sale-and-leasebacks. Still others wonder how China’s lessors, which have grown during a robust run of passenger growth and record low interest rates, may fare in a downturn, especially those without the experience of Western lessors that have weathered those conditions before.

For now though, it appears that little will slow the continuing rise of Chinese lessors in the global aviation finance market.

Follow us for more FlightGlobal news and data on WeChat:

Source: Cirium Dashboard