Much has been made about the fresh generation of widebody aircraft opening up new international gateways in cities such as Austin, San Diego and San Jose, with routes to faraway cities such as London and Tokyo.

These airports have seen gains. International seats have nearly doubled at Austin between 2011 and 2015 and all three are able to offer travellers nonstop options to markets that were only reachable via a connection in a major hub or gateway.

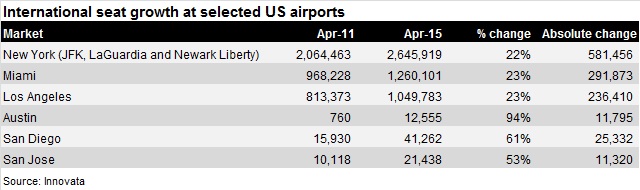

This may sound like progress, but dig into the numbers and the Austins, San Diegos and San Joses of the USA have seen only a fraction of the new international capacity that has been added during the past four years.

Together, the three airports only gained 48,447 international seats. This represents a 180% increase for them but makes up less than 2% of the 2.7 million international seats that were added nationally from April 2011 to this April, Innovata FlightMaps Analytics data shows.

New York, Miami and Los Angeles – already among the largest and best-known gateways to the USA – landed the lion's share of new international capacity. Together, they gained more than 1.1 million seats, or nearly half of all the international capacity growth in the country, during the period.

Looked at another way, New York, Miami and Los Angeles together gained the equivalent of one Emirates Airbus A380 flight per day compared to one more 50-seat regional jet flight in Austin, San Diego and San Jose.

BIG TO BIGGER

“You start building it, you amass more and more connectivity and it’s just easier to add more capacity,” says Brad DiFiore, managing director at air service development advisers Ailevon Pacific, citing the massive number of connecting opportunities each city offers carriers.

New York, Miami and Los Angeles each have what carriers want. First and foremost, they are large origin and destination markets that have sizeable existing passenger bases. Second, and to DiFiore’s point, they are each large hubs for the US mainline carriers providing them and their alliance partners significant beyond connectivity.

New York JFK International and Newark Liberty International airports are either major hubs or key focus cities for four of the USA’s six largest carriers: American Airlines, Delta Air Lines, JetBlue Airways and United Airlines. One way they compete with each other for share is by offering broad domestic and international networks.

JetBlue added nonstop service to three – Cartagena, La Romana and Samana – of the 10 new routes that New York gained in the past four years, Innovata data shows. This was part of a broader strategy of expansion to the Caribbean and Latin America out of the market, which former chief executive David Barger told Flightglobal in June 2014 “mature [more] quickly” than new domestic routes.

The hometown carrier is investing in its international growth. It opened a roughly $200 million international arrivals facility in Terminal 5 at JFK in November, eliminating the need for arriving flights to deplane in Terminal 4. This improves efficiency and reduces expenses for the airline.

Competition between American and Delta, as well as their transatlantic joint venture partners British Airways and Virgin Atlantic Airways, drove a 23% increase in seat capacity to what was already New York’s largest international market: London.

Delta and Virgin Atlantic have together increased the number of seats they offer in the market by nearly a third to roughly 94,000 this April since 2011, Innovata shows. While still second to American and BA in the market, they are much more competitive with a co-ordinated schedule and co-located gates at both JFK and Heathrow.

Executives at Delta have repeatedly said that they were at a competitive disadvantage in New York because of their lack of adequate London Heathrow access. This prompted the purchase of a 49% stake in Virgin Atlantic in 2013 and the launch of the joint venture in January 2014.

“Virgin Atlantic gives us access to London Heathrow in the most lucrative, most heavily travelled market, JFK to London Heathrow,” said Paul Jacobson, chief financial officer of Delta, following the launch of their joint venture in March 2014. “Now we have a schedule that allows us to complete with the American-BA alliance in the New York to London travel market.”

Many foreign carriers have also increased capacity or added new routes from New York. For example, Delta’s SkyTeam partner Aeromexico launched Monterrey service in December and its partner, China Southern Airlines, added Guangzhou service in August 2014. United’s Star Alliance partner Austrian Airlines began service to its Newark hub from Vienna in July 2014.

Los Angeles (LAX) is a similar story. American, Delta and United all jockey for the leading position at the airport with the latter holding the top spot by 2.3 percentage points with an 18.3% share of passengers in 2014, operator Los Angeles World Airports data shows.

The market offers significant local corporate sales opportunities and a high level of international feed. These opportunities drove at least part of the 29% increase in international capacity at LAX to 1.05 million seats from April 2011 to April 2014, Innovata data shows.

During the four-year period, American added new service to Edmonton, Sao Paulo and Vancouver; Delta added Belize City, Liberia, London, five new destinations in Mexico, San Jose (Costa Rica), San Salvador and Vancouver; and United added Durango (Mexico), Melbourne (Australia) and Shanghai.

London is as much a battleground from LAX as it is from New York. American and BA increased their seat capacity by 44% to 51,000 seats, Delta and Virgin Atlantic by 64% to 27,800 seats and United – the smallest in the market – by 18% to 9,375 seats from 2011 to 2015, Innovata data shows. The growth came from a shift to larger gauge aircraft. BA shifted its flights to Airbus A380s, and an additional frequency, and American added a second daily flight this March.

In addition, European low-cost carrier Norwegian launched twice-weekly service between LAX and London Gatwick in July 2014. It also began Copenhagen, Oslo and Stockholm service from the Southern California airport the same year.

Asian alliance members are big drivers of growth at LAX. For example, American’s Oneworld partner Cathay Pacific added a fourth daily flight from Hong Kong in June 2014, Delta’s SkyTeam partner Korean Air increased frequency from Seoul in March 2014 and United’s Star partner Air China began a second daily flight from Beijing in September 2011.

LAX has improved its facilities to support new service. A multi-billion dollar overhaul of the Tom Bradley International Terminal is scheduled for completion this year and Terminal 2, the airport’s second largest international arrivals facility, is undergoing a full revamp scheduled for completion in 2017.

Miami stands apart from both New York and LAX. Much of its international growth is driven by its largest carrier, American, which operates nearly 70% of seats from the airport, and from being the primary US gateway for numerous Latin American carriers, including the largest in the region LATAM Airlines Group.

Fort Worth, Texas-based American is responsible for six of the 13 new routes added at Miami during the four years ending this April, Innovata shows. LATAM subsidiary TAM – also a member of Oneworld with American – is responsible for another two routes to Curitiba and Fortaleza.

Existing markets also grew. Seats to Sao Paulo – already the largest international market from Miami – more than doubled to 35,573 as American shifted to larger Boeing 777-300ERs from 777-200s on the route, and Punta Cana saw a near 250% jump to 25,062 seats as American increased frequency and Brazilian low-cost carrier Gol selected it for its one-stop service from Brazil.

Miami, like New York and LAX, recently completed a round of capital investments. A new international arrivals facility in concourse D, which is home to American’s hub, fully opened in 2014 and a new South Terminal, which hosts LATAM, as well as SkyTeam and Star member flights, opened in 2007.

POWERFUL ALLIANCES

The growth in capacity at these major gateways follows an increase in “hub-to-hub” international flying. The trend of funneling more passengers through partner hubs has accelerated in recent years with Delta flying more than half of its peak season transatlantic capacity into the hubs of its joint venture partners – Air France, Alitalia, KLM and Virgin Atlantic – for the first time in 2014.

“We are in a unique position to collaborate with our joint venture partners to make full use of our combined fleet and networks to best serve our customers," said Glen Hauenstein, executive vice-president and chief revenue officer of Delta, in May 2014. "Delivering more hub-to-hub flying provides a network with higher frequencies and tailored schedules for our transatlantic travellers.”

This trend appears to have accelerated at Heathrow. Independent of their partners BA and Virgin Atlantic, American and Delta increased capacity by 30% to 154,000 seats and 22% to 84,000 seats, respectively, at the airport from April 2011 to this April, Innovata shows.

American, BA and US Airways together added about 129,000 seats for 546,000 between Heathrow and the USA, and Delta and Virgin Atlantic added about 63,000 seats for 241,000 in the market during the period. However, these numbers include routes to US spokes, for example Austin on BA and San Francisco on Virgin Atlantic.

“We are seeing some success in the corporate market with customers…especially in the major gateway areas of New York and Los Angeles,” said Chris Rossi, senior vice-president of North America for Virgin Atlantic, in July 2014, echoing the corporate travel advantages cited by Jacobson.

Other European hubs also saw dramatic capacity increases. American and US Airways increased seats by nearly 9% to their partner Iberia’s Barcelona and Madrid hubs, Delta increased seats to Air France and KLM’s Paris Charles de Gaulle and Amsterdam Schiphol hubs by 50%, and United increased seats to Lufthansa’s Frankfurt and Munich hubs by nearly 15% during the period, Innovata shows.

Latin America and Asia have yet to see the same level of hub-to-hub flying between partners. This is largely the result of fewer, or less mature, joint ventures in the market, compared to the transatlantic where Northwest Airlines (absorbed by Delta in 2009) and KLM forged the first such partnership in 1997.

American has immunised partnerships with Japan Airlines and Qantas Airways, and United with All Nippon Airways across the Pacific. Delta and Aeromexico hope to forge the first joint venture between the USA and Latin America in 2016. Other than these partnerships, airlines rely heavily on codeshares and expanding their own networks in the regions – driving much of the international growth at smaller US airports.

NEW GATEWAYS

Austin, San Diego and San Jose are all relatively new US international gateways. Austin only received its first ever nonstop to Europe when BA began its London Heathrow flight in March 2014, and San Diego got its first flight to Asia when JAL began its Tokyo flight in 2012.

ANA’s Tokyo-San Jose flight restored a route operated by American until 2006, which the Oneworld carrier dropped citing high fuel costs and low demand at the time.

These new gateways are not without their partner connections. BA and JAL’s partner American has a strong presence and good sized pools of frequent flyers in both Austin and San Diego, while ANA is able to leverage its partner United’s corporate relationships and frequent flyer base as the largest in the San Francisco Bay Area, which includes Oakland, San Francisco and San Jose airports.

Not every airport has seen more international service. Places like Cleveland, Memphis and Pittsburgh have seen declines in their international seats as United, Delta and American subsidiary US Airways have cut their respective hubs at the facilities in recent years.

International traffic is not so different from the rest of the US airline industry in recent years. Consolidation has allowed carriers to grow at the biggest airports and, outside those, new capacity is focused on places that are bright spots in the economy, largely in the south and west.

Source: Cirium Dashboard