The relentless rise in mainline jet output continued in 2017, with Airbus and Boeing both setting new production records and reaching almost 1,500 deliveries between them. There has also been a significant uptick in orders – which was not forecast a year ago – and the outlook for the near term at least remains positive.

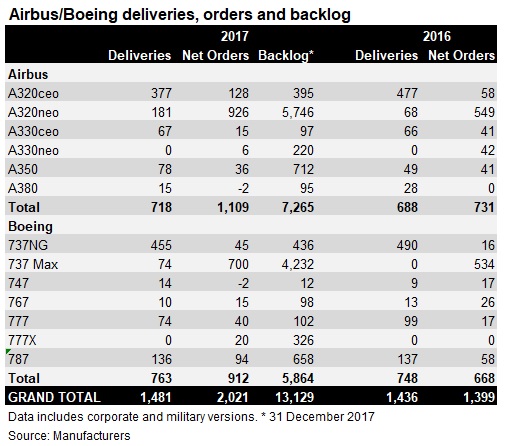

Airbus saw a 4% increase in deliveries to a personal best of 718 aircraft in 2017 and the manufacturer's commercial aircraft president Fabrice Bregier expects a further increase to "close to 800" deliveries this year. Boeing's output also broke records – its own and the industry's – but only by one unit. The OEM shipped 763 aircraft – up 2% on 2016's 748 deliveries, but only slightly ahead of its previous all-time record of the 762 it delivered in 2015. This put combined 2017 deliveries at 1,481 – 3% higher than 2016's 1,436.

Airbus's 2017 production was close to its original target from a year ago – which was set prior to the industrial problems that engine supplier Pratt & Whitney suffered during 2017. This impacted A320neo deliveries, resulting in "60 gliders" in storage awaiting engines, says Bregier.

By year-end, half of these had been delivered. Airbus handed over a total of 181 A320neos (73 Pratt-powered and 108 with CFM International engines), compared with 377 A320ceos. Bregier is confident that if clear of any further engine industrial issues, A320neo deliveries will this year transition from the one-third share of all A320 shipments in 2017 to nearer two-thirds.

Airbus has now trailed Boeing in overall output for the past six years. However Bregier expects this position to be reversed by 2020. Forecasting that Airbus single-aisle production will be “well above rate 60 in 2019” with “much greater potential beyond that”, Bregier says he bets “in 2020 that Airbus will become the leader in not only the sales, but also the deliveries”.

The rise in overall output was driven entirely by narrowbody demand as deliveries of widebodies actually declined slightly year-on-year through cuts at Boeing. A320 and 737 deliveries rose 5% in 2017 to a combined 1,087 units, with Airbus just getting its nose ahead.

Although it reduced overall widebody output, Boeing continues to dominate this arena. Despite Airbus pushing up twin-aisle output by over 10% to 160 aircraft, its US rival still delivered close to 60% of widebodies (234 units). Overall, combined widebody shipments declined by seven units, largely as a result of 777 production falling by a fifth along with flat output on the 787 line.

From a sales perspective, 2017's tally of 2,021 net orders makes it the sixth year ever that net sales have exceeded 2,000 units. It is the highest annual order total since the all-time record of 2,888 net orders in 2014, and the fifth consecutive year that Airbus has been overall market leader. Toulouse's 1,109 net orders represent a 55% share.

The industry's full-year sales performance – which beat predictions made at the start of last year – restored the overall net book-to-bill ratio to the healthy level of more than 1.3, after its decline to less than one in 2016.

"The market is just stronger everywhere," explains Airbus chief operating officer for customers John Leahy. "The stock market is stronger, the economies of the world are all firing at the same time in the right direction, and IATA's telling us that air traffic should be about 7% up. Yeah, and airplane orders are stronger than we thought at the beginning of the year. And it should spill off into 2018 – we would think we'll still maintain a book to bill of one.”

Rob Morris, head of Flight Ascend Consultancy, is not convinced that current economic drivers alone have propelled orderbooks higher, given the very long lead times for deliveries: "Perhaps airlines and lessors are getting caught up in the hysteria of this increasingly long and high growth cycle, which is causing them to commit to orders for delivery in several years' time without thinking through the risk in the cycle," he says.

"If airlines and lessors are willing to so commit, then of course Airbus and Boeing will take the orders and take some element of certainty in their future volumes and pricing. While there appear no warning signs on the horizon yet, the sun cannot continue to shine forever."

Airbus strengthened its position in the single-aisle market with the A320 taking 58% of the orders. In overall terms, single-aisle sales surged by over 50% to 1,799 orders.

"Perhaps [Airbus's strong performance] is some continued reflection of the A321 position compared with the 737 Max 9/Max 10, where even the launch of the latter seems not to have slowed the Neo order momentum," says Morris. "I guess this will exert further pressure for a Boeing NMA [New Mid-market Airplane] launch, or at least authority to offer, in 2018."

Overall, sales in the widebody sector declined year-on-year to 222 net orders. Boeing more than compensated for being shaded in single-aisles with a whopping 75% share of widebody net orders. This was driven largely by a strong order performance from the 787 (94 net) and 777/777X (60), with the deal for 40 787-10s announced by Emirates at the 2017 Dubai air show yet to be counted.

The sales performance across the Airbus widebody product line was disappointing last year, with net orders declining to 55, from 124 in 2016. The A330neo, which is currently in flight-test, gathered just six net orders.

"Airbus must be concerned about lack of A330neo momentum because comments at the start of last year indicated that they saw this as a priority in 2017," says Morris. "With the relative weaker performance for the A350 also, Airbus must be increasingly concerned about twin-aisle market performance in 2018 and beyond."

The situation on the A380 remains dire, with the programme seeing a contraction in its orderbook by two aircraft. Bregier concedes Airbus has "a commercial challenge" on its widebody flagship, while Leahy is blunter, saying that if the hoped-for order from Emirates does not materialise, there will be "no choice but to shut down the programme".

However, Leahy is more upbeat about the prospect of short-term widebody sales, saying Airbus has "about three widebody deals that I would hope we could sign within the next 30-60 days – watch this space".

In overall terms, the two commercial aircraft giants' strong sales performance caused the industry backlog to rise again after the blip in 2016, growing by over 4% to 13,129 aircraft at 31 December 2017. Based on current rates, this equates to around eight years of production.

Source: Cirium Dashboard