As seriously as a monk takes their vows, Australia’s two airline groups have been adhering to the mantra of capacity discipline – with strong results to prove it.

Qantas issued profit guidance in early May showing that it expects a new record full-year profit before tax of up to A$1.6 billion ($1.2 billion).

“We’re seeing solid results from each of our business units, which is a reflection of broadly positive trading conditions and the work we’ve done to strengthen the group,” commented Qantas group chief executive Alan Joyce.

It’s quite a turnaround from 2014 when the carrier reported a net loss of A$2.8 billion, as a capacity war against rival Virgin Australia, a major writedown against the value of international fleet, and tough international conditions saw it report the worst result in its nearly 100 year long history.

Virgin, meanwhile, is further back on the turnaround curve, but has seen a return to profit for the half-year to 31 December of A$103 million.

“This demonstrates the success of our long-term strategy to reposition the business and strengthen its financial foundation; however there is more work ahead to ensure we continue to delivery,” says chief executive John Borghetti.

The once cheap-and-cheerful carrier has transformed into a more business-focused airline, and one that competes across all customer segments with the larger Qantas group.

Both carriers have seen demand growth in the key domestic market slow to single-digit rates in recent years, largely due to slowing economic growth, lower business confidence and a downturn in commodity prices, which impacted corporate travel.

That forced both carriers to cut back capacity on some routes, with Qantas and Virgin both redeploying widebody capacity from the domestic market to international routes. Virgin also cut its Embraer 190s from the fleet, and reduced the number of ATR 72 turboprops it operates, replacing some of those with aircraft wet-leased from independent operator Alliance Airlines.

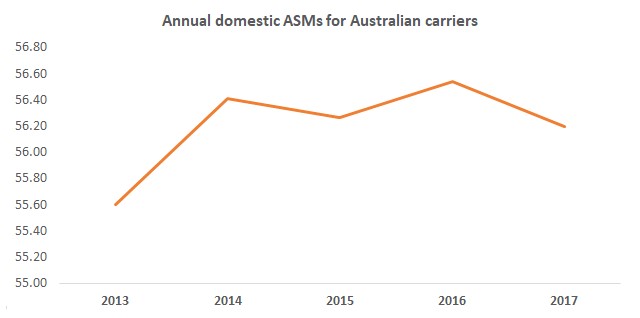

Source: FlightGlobal schedules. Units in billions of ASMs

Conditions are strengthening now however, with corporate and leisure travel both growing again. The latter includes an uptick in premium leisure demand, which has seen some routes that were previously the domain of the budget carriers moved back to their mainline ones.

While Virgin has moved back into the black, it is still emerging from the damaging competition of the 2012-14 period with Qantas that savaged its balance sheet.

Its search for cash saw the acquisitive HNA Group inject close to $1 billion of equity into it last year, while long-term partner Air New Zealand sold out its stake to another Chinese conglomerate, Nanshan Group, in 2017.

That leaves it with a complicated, multi-airline ownership structure. Etihad Aviation Group holds the largest stake at 25.1%, followed by Singapore Airlines (20.1%), Nanshan (19.9%) and HNA (19.2%).

INTERNATIONAL NICHES

Similarly, on the international front, both Qantas and Virgin Australia have been restrained as they work among the realities of being at the end-of-the-line.

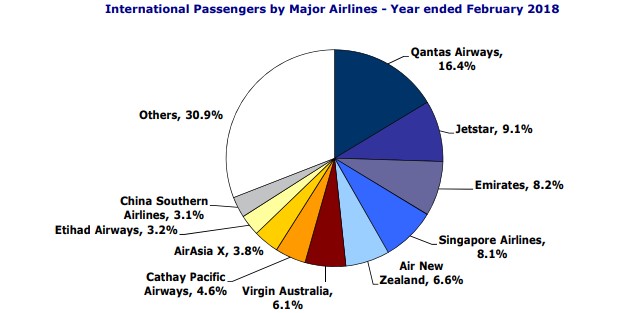

Qantas still holds a commanding share of the fragmented international market, with 16.4% of international passengers for the year ended February 2018 taking the Flying Kangaroo. Subsidiary Jetstar was the second largest at 9.1%, followed by Emirates, Singapore Airlines, Air New Zealand and Virgin.

Image source: Commonwealth of Australia/Bureau of Infrastructure, Transport & Regional Economics

That has seen their networks largely coalesce around major partnerships to serve key markets. Qantas works closely with Emirates, American Airlines and China Eastern, while Virgin with shareholders Singapore Airlines, Etihad Airways, HNA Group and Air New Zealand. Virgin also has a joint venture with Delta Air Lines covering North America.

But Virgin is set to lose one of its key partners in October, with Air New Zealand recently calling time on transtasman joint venture. The Star Alliance carrier has announced a major increase in capacity, aimed at plugging the effective gap from the end of the codeshare with Virgin.

That change follows some wider changes on the Tasman market, with Emirates ending its A380-operated tag services from Melbourne, Brisbane and Sydney to Auckland in March as it concentrates on its nonstop Dubai-Auckland service. Alliance partner Qantas has back-filled some of that using A330s and 737s.

After years of pulling back, Qantas’s international network has started growing again, with the debut of nonstop services to Europe through the Perth-London route in March. At the same time, it operated its last services to Dubai and rerouted its Sydney-London services back via Singapore.

The Oneworld carrier has signaled that longer nonstop flights will be a major part of its future, with the carrier set to examine an order for aircraft that could fly from Australia’s east coast to Europe and the US east coast set to be placed next year.

Closer to home, Virgin’s limited international network focuses on the US, Pacific Islands, and last year it launched Melbourne-Hong Kong flights. From July it will commence flights from Sydney to Hong Kong, which, like the Melbourne ones, will be underpinned by its alliance with the HNA Group, and its Hong Kong Airlines unit.

Virgin is also looking to launch a mainland China destination, but as chief executive John Borghetti said in February, is facing difficulty getting slots at key gateway cities there.

“With our expansion into greater China, it’s also the art of what’s possible. We’re talking about airports that are very congested: Hong Kong, Shanghai and others,” he said,

Qantas has similar benefits from its joint venture on China routes with China Eastern Airlines, which is supplemented with a codeshare agreement with China Southern Airlines.

Those agreements have helped the carriers to gain exposure to the surging Chinese tourist market, which has seen a number of carriers including Hainan Airlines, Tianjin Airlines and Xiamen Airlines launch new services to Australia over the past three years.

BUDGET BOOM

Australians have developed a strong penchant for overseas travel, which in part has fueled a large rise in low-cost carrier capacity to the country.

Asia’s long-haul low-costers AirAsia X and Scoot have both deployed large amounts of capacity to Australia. The latter also sees Australia as a key connecting market for its European services, and has offered very attractive fares connecting Australian passengers through Singapore to Athens.

Filipino carrier Cebu Pacific Air has also received warm welcome in Australia, with its 440-seat, all-economy configured A330s plying the Sydney-Manila route five times a week. In August it will add a thrice-weekly flight to Melbourne.

Qantas and Virgin’s budget brands have also been strong contenders in the international market. Jetstar plies a number of routes to destinations including Denpasar, Osaka and Honolulu. Tigerair Australia operated a number of services to Denpasar until early 2017 when it ran afoul of Indonesian regulators. It is now expected to start services to New Zealand.

Source: Cirium Dashboard