Business jet prices are still falling - but approaching stability after two years of significant declines. However, overall market conditions remain depressed and have dipped slightly since January, indicating a stalled recovery, with high inventory levels remaining a drag on business.

These are key findings from March, in UBS global equity research's bi-monthly survey of US and international business jet brokers, dealers, manufacturers and financiers.

When asked about overall business conditions, responses ranged from zero (worst ever) to eight (with 10 being best ever) for a market score of 3.6 (where five is normal). The scored dipped below five in the September 2008 survey and slid as low as 2.2 in March 2009 before beginning to recover. But, this March, sentiment slid back from January's 3.7, indicating that recovery has stalled.

Further evidence of a stall came as most respondents in March said customer interest in new or used jets was improving - but fewer are seeing signs of improvement than in January. But as with overall business conditions, the US market seems to be faltering while, internationally, conditions are still edging upwards.

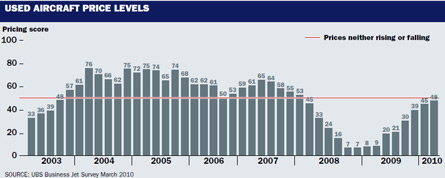

When asked whether overall pricing levels had increased, decreased or stayed the same since January, a rising number of respondents reported that prices had stayed level or risen. That translates into a market score of 48, where 50 would indicate price stability.

So prices continue to fall month-on-month, but the rate of decline is, finally, approaching zero. The UBS results show a steady march back towards stability from a nadir reached in November 2008, after prices plunged precipitously beginning in January 2008.

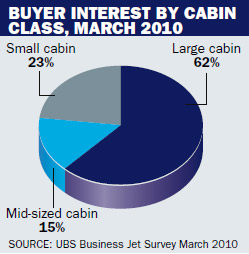

The latest UBS survey also backs up much anecdotal evidence that it is in the large-cabin class that prices are strongest and buyer interest is greatest.

Looking forward, just 4% of respondents expect overall business conditions to deteriorate over the next 12 months, with the rest predicting improvement or stability. The UBS score on this count came in at 79, down from 82 in January, but still well above the 50 mark, which would indicate expectations of neither improvement nor deterioration.

Where brokers and dealers indicate some cause for alarm, however, is in inventory levels. In the March survey, 92% of respondents said inventories were high - up from 88% in January - and the oversupply of young, high-quality used aircraft remains significant. However, feeding a sense that the near-term outlook is positive was an increase in the overall willingness of traders to increase their inventories.

And, survey respondents continue to report increasing availability of customer financing. That availability has been increasing rather than decreasing since May 2009.

Indicative of the tentative nature of market recovery are comments from some of the respondents, as highlighted by UBS analyst David Strauss:

Source: Flight International