Among the inevitable Le Bourget buzz about aircraft sales and new technology will be one key piece of will-they-or-won't-they? Safran and Thales, two of the biggest names in French aerospace, are formally in negotiations about "asset swaps".

After several years of on-off talk of a merger or other tie-up, there's no cause to expect a rush to seal an agreement in time for a Paris air show announcement, but while both will be prominent exhibitors the main interest may be in what they are up to behind the scenes.

Neither company is saying anything beyond confirmation that they are talking. It is believed, though, that asset swaps could involve Thales getting some optical sensor businesses with such capabilities as night vision in exchange for some security and avionics-oriented businesses.

|

|---|

What is not known is whether the pair are also considering any wider alliance or even merger, and whether the French state, which is a major shareholder in both, is driving the negotiations. But both of those questions loom large over the wider French aerospace industry, which like its counterparts in the developed world is facing a transformative storm of forces including new competition from rising economies and shrinking defence budgets at home.

FRENCH APPROACH

Dassault's €1.57 billion ($2.26 billion) purchase of a fifth of Thales from ailing communications giant Alcatel-Lucent in 2009 probably says as much as needs saying about the French approach to its aerospace and defence companies. The deal made sense, as the two companies have a long history of working together. Thales, primarily focused on defence electronics, is a key supplier to the Dassault Rafale fighter used by the French air force and navy and now on the two-aircraft shortlist, with Eurofighter, for India's much-coveted strike jet contract.

The deal also kept Thales in French hands, leaving Dassault and the French state between them controlling the company. The only other likely bidder was Airbus parent EADS, which like Dassault is long on cash but at that time was too wrapped up in its Airbus Military A400M transporter travails to spare much thought to a major acquisition.

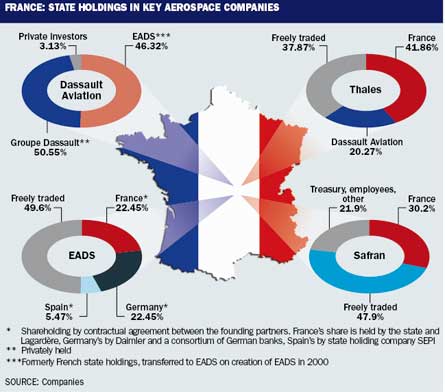

As the chart on this page shows, the French state remains an active shareholder in several of the big French aerospace players and is heavily tied in to both Dassault Aviation and EADS, with its heavy-fifth shareholding in the latter carefully balanced by German holdings. The French-German balance in EADS stems from that company's creation in 2000 from various state holdings and national champions of the two countries that had joined forces in the late 1960s to create Airbus.

But while Paris protects its interests in EADS and values the Airbus position as a global leader in civil aviation, on the defence side the partnership with Dassault clearly prevails. The existence of Rafale, which is similar to the EADS-led Eurofighter, proves as much. With Dassault Aviation, the government holds a short half of the company otherwise owned by privately held Groupe Dassault whose chief executive, Charles Edelstenne, is one of the richest men in France.

FRANCO-FRENCH DEAL

The prospect of a major merger or acquisition - the so-called "Franco-French deal" to create a mega-player, as one London analyst puts it - looks unlikely. EADS, of course, is ultimately the product of a merger. But while Paris and Berlin paid much attention to establishing a balance between their interests when they tied the knot, by 2000 the constituent parts of the company were, in practice, acting as one and so the creation of EADS was, in effect, a marriage that followed many years of successful cohabitation. Occasional whispers of an EADS move to absorb Safran or Thales have never gone beyond the rumour stage, and smell more of idle musings by fantasy merger and acquisition players than any real consideration inside corporate headquarters.

|

|---|

© Dassault |

The French state is a minority shareholder in fighter and business jet maker Dassault |

Safran, too, was created by merger with the 2005 union of Snecma - whose roots go back to 1905 and the Gnome aero engine business, and is GE's 50:50 partner in the hugely successful CFM International civil engines venture - and Sagem, the mechanical engineering, defence electronics and telecoms group. Safran soon divested its mobile phone and broadband businesses to focus on its core aerospace and security businesses, a decision that many defence-heavy rivals must admire as they look enviously at the growth potential of the homeland security sector.

The history of corporate mergers and major acquisitions is littered with colossal failures, so the apparent success of the Snecma-Sagem marriage is a rarity - in 2010 Safran made €508 million on €10.8 billion sales - and EADS chief executive Louis Gallois has made it very clear that while the company is always interested in small, tactical acquisitions, anyone waiting for a big, transformative deal should stop holding their breath. As he considered buying Alcatel's Thales stake in 2009, Dassault's Edelstenne ruled out a full takeover, noting that cultural and other differences led 60% of such deals to be failures.

Thus the appeal of Thales-Safran "asset swaps"; without the risk and expense of merging large companies, both may be able to ramp up their competitiveness by improving their technological, product and customer focus. Safran is already strong and while Thales lost €100 million in 2010 after taking a remarkable €700 million charge against troubled supply contracts including with the Airbus Military A400M, its problems do not look insoluble and chief executive Luc Vigneron, who took the helm in 2009 after Dassault's buy-in, looks to have a viable plan for turning the group around.

However, there is clear impetus for a French industry consolidation, at least on the defence side. Professor Joseph Lampel of City University London's Cass business school notes that the French see themselves as having, potentially, Europe's most powerful defence industry but know their companies have to grow to be world players, given the rise of competition from the likes of Brazil, China and India.

And, he adds, France is not alone in needing to encourage its defence industry players to press for scale if they are to be the principal suppliers to their domestic armed forces. Even the US government, he says, is not a big enough customer to support US firms' research and development spending without export sales. The French government, says Lampel, is "no doubt" playing a behind-the-scenes role in pressing for some industry restructuring.

France's increasingly internationalist foreign policy - see its re-engagement with NATO and willingness to take a lead, as in Libya this year - is creating both opportunity and challenge for French arms makers. The opportunity comes in greater interest from export customers and the challenge is in surviving as France, inevitably, opens up to more purchases of foreign-made equipment as it looks to maximise value for money in defence spending.

Thus, says Lampel, French industry has to respond: "The economics of defence procurement is just too punitive with industry as it is."

Aerospace and defence drive exports

Aerospace, defence, electronics and security is France's leading industry sector in exports and profit, contributing some €18 billion ($26 billion) to the country's balance of trade, according to industry association Gifas.

And, says Gifas chairman Jean-Paul Herteman: "On the employment front, despite the economic crisis we took on 8,000 workers in 2010, raising the total workforce to 157,000, and have recruited 27,000 people since 2008."

In 2010, industry revenue rose by 3.5% to €36.8 billion, with 73% of that being exports, thanks largely to civil business. Air transport led a 27% rise to €42.9 billion in the French industry order book, with the civil sector accounting for 71% of orders. For the seventeenth consecutive year, orders exceeded revenues and now stand at four years' output.

For equipment manufacturers, says Herteman, "the recovery started to take shape in 2010". Revenues were down 4.8% at €9.2 billion, but a 34% increase in orders, driven by the civil aviation sector, "bodes well for the sector as a whole", adds Herteman.

In the space industry, revenue edged down slightly to €4.2 billion.

Source: Flight International