Chris Seymour, head of market analysis at Flight Ascend Consultancy, examines the future shape of Latin America’s fleet

The airline fleet in Latin America, including Central America and the Caribbean, has averaged 2.2% annual growth over the past 20 years, and its 2,100-strong fleet is now 8% of the global total.

The fleet is forecast to grow faster, by 3.8% annually, in the next 20 years, which will lead to 2,350 additional aircraft and take the fleet to almost 4,500, increasing its share to 9% of the global total. Although the region is suffering from Brazil’s current recession, longer-term growth prospects are strong.

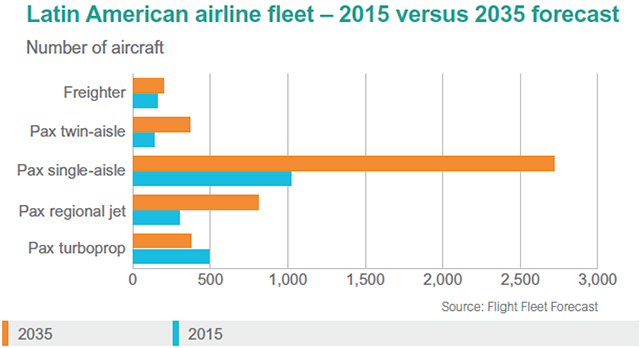

Some 92% of the fleet is currently used in the passenger market and 8% is for carrying cargo; this balance will change to a reduced 4% cargo share by 2035, as available belly space is growing faster than the need for main-deck freighters.

Latin America’s airlines have seen a significant increase in deliveries in the past five years, with 680 aircraft for replacement and low-cost carrier growth. Once the short-term downturn in some markets is overcome, the region is forecast to continue these higher rates of deliveries, with 3,785 new aircraft in the next 20 years, a 9% share of global deliveries.

This includes some 3,525 passenger jets, 240 passenger turboprops and 20 freighters. The jet total includes more than 2,400 single-aisle aircraft and 350 twin-aisles. About 75% of the current fleet will be replaced, but almost 60% of deliveries will be for growth.

Latin America’s fleet is predicted to remain focused on the single-aisles over the forecast period, with a current 48% share of the total fleet rising to 61% by 2035. Regional jets will increase their share by four points to 18% and twin-aisle types will rise a point to 8% of the fleet. The freighter fleet will also increase slightly, but its share will fall to 4% of the total fleet, and the turboprop share is set to decline from 23% to 8% as the overall fleet is reduced.

Latin America and the Caribbean is one of the key passenger growth regions for the future, with increasing leisure traffic stimulated by low-cost carriers and continued liberalisation in major markets.

The growth of low-cost airlines, which began in Brazil, is now spreading to other countries such as Mexico, with low fares tempting traffic away from buses. Airline groups such as LATAM and Avianca are also aiding fleet expansion in smaller countries across the region. The passenger jet fleet is predicted to grow by 5% annually over 20 years to 3,890 aircraft.

With a fleet of just over 300, the regional jet has seen a major resurgence in the Latin American market in the past 10 years, with orders, mainly for Embraer, from both Central and South America, and the Sukhoi Superjet selling into Mexico. FlightGlobal predicts some 750 new regional jet deliveries, increasing the fleet to more than 800 by 2035. The majority in the forecast are 100-seater types, replacing 245 older regional jets and also some older generation single-aisles.

Some 64% of the new deliveries are forecast to be single-aisle jets, with these 2,400 aircraft taking the fleet to 2,700 by 2035. The 150-seaters feature predominantly in the forecast with 1,840 deliveries, although in the 2020s, the larger 180-seaters will take an increasing share of annual deliveries, and by 2035 will have a 20% share of the total deliveries. The low-cost carriers will be the key drivers of single-aisle deliveries throughout the forecast.

The twin-aisle passenger jet fleet of 140 is forecast to grow by 4.9% a year to some 370, with 350 new deliveries (more than a third for replacement). The delivery focus is on the smaller sizes (36% for 200- and 250-seaters and 42% for 300-seaters), with types such as the Boeing 787 and Airbus A330 to mainly serve the US markets, and 777s, A330s and A350s for Europe and some routes into Asia. The higher-capacity 350-seaters begin to have significant annual deliveries only in the second half of the forecast, and no demand is predicted in the large category.

The Latin American passenger turboprop fleet has a 14% share of the global total, and major turboprop markets include Brazil, Colombia, Venezuela, Mexico and the Caribbean islands, where turboprops are the most economic for inter-island hops.

MORE SEATS

Although the fleet has remained at about 500 aircraft in the past decade, it has seen a change in size share, with 70-seaters being added for new networks, especially in Brazil. The forecast is for 240 deliveries in the next 20 years, with the fleet dropping to 375 as the smaller seat sizes are phased out. By 2035 all but 70 of the fleet will be of the 50-90 seat size.

The freighter fleet increased slightly in the past five years to 160 and is forecast to grow by just over 1% annually to reach 200 aircraft by 2035, with 20 new deliveries and 136 conversions allowing more than 80% of the current fleet to be replaced.

There has been more focus on newer-generation types such as the 777F and A330-200F, especially to carry perishables to the North American market. Two-thirds of the fleet comprises narrowbodies and turboprops serving short-haul markets, and the conversions will help to renew this fleet, with the 737, A320 and ATR at the forefront.

To find out more and download the Flight Fleet Forecast summary, click here

For coverage of the ALTA Airline Leaders Forum taking place in Mexico City on 13-15 November, visit www.flightglobal.com/alta

Source: Cirium Dashboard