Ascend's head of consultancy Rob Morris weighs in on recent suggestions that the assumed economic life of an aircraft should be reduced to 18 years

Shortening assumptions on the economic useful life of aircraft has some merits, but recent suggestions that it could be as short as 18 years are likely too aggressive.

At the recent ISTAT Asia event in Singapore, Apollo Aviation president Robert Korn brought the issue into focus, calling for the industry to adopt much more conservative assumptions on residual values and depreciation. He noted that Apollo does its modelling on an 18-year depreciation to a 10% residual value, compared with the industry norm of 25 years to a 15% residual.

Flightglobal's Ascend Fleets database shows that historically, the average economic lives of aircraft that have been permanently retired have reduced from around 32 years in 2008 to an average of 26 years in 2014. More recently, however, there have been a number of types that have been tracking below that lifespan, as some carriers move to churn their fleets more regularly, in part to benefit from newer, more fuel-efficient aircraft.

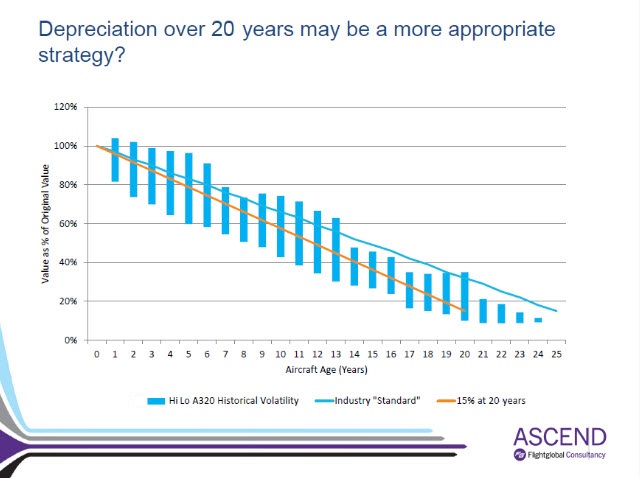

Further empirical evidence does support reining in the assumed economic life of an aircraft. Ascend data on A320 values' volatility plotted against the prevalent 25-years-to-15% residual assumption puts that depreciation profile at the upper end of that volatility band, exposing the aircraft investor to more downside risk than upside opportunity.

It is therefore Ascend's view that a 20-year depreciation to a 15% residual value may be a more appropriate course of action. On the same plot, that puts it in the middle of the volatility band, and keeps up- and downside risk relatively balanced at 50% either way – allowing greater certainty for investors across the business cycle.

Economic lives started to compress in the last demand-led downturn around 2009. Through that reduction in demand, manufacturers kept production steady, leading to some surplus of new aircraft. When combined with low borrowing costs, airlines and investors opted to continue to accept delivery of these newer aircraft, displacing the older and less efficient aircraft from the fleet earlier than their assumed 25-year life. As a result, a number of lessors were forced to take impairments on aircraft that ended up being sold, typically for part-out, before the natural end of their economic life.

With the industry now in full recovery from that downturn, demand fundamentals are strengthened and new aircraft are once again required for growth rather than replacement. Even with global economic growth continuing below trend, overall demand for air travel continues to grow strongly, pushing up airline profits. Even the most cynical of observers are finding it hard to spot any potential roadblocks to that growth in the short term, barring the metaphorical "black swan" event.

In that environment, more carriers have been adding new capacity and, in many cases, also renewing leases on their older aircraft to keep up with the competition.

Nowhere has that been more demonstrated than North America. United Airlines and Delta Air Lines are both moving to expand their fleets by leasing or acquiring older aircraft from other operators. In some cases, aircraft are far exceeding the 25-year limit. European flag carriers such as British Airways and Lufthansa have also tend to retain their fleet for a longer period, compared with Middle Eastern and Asian carriers which have 12-year depreciation policies.

The low cost of financing and growth in operating leasing is also another factor that should hold back any major changes to depreciation policies. Thanks to US monetary policy, liquidity is now much more available than in the global financial crisis, and low yields in other asset classes have pushed more money into aircraft lessors. Today, around 40% of aircraft are owned or managed by lessors.

It is those lessors and investors for whom changes in depreciation policy have the largest impact, as they ultimately bear the risk on aircraft assets. A lessor looking to shorten its depreciation policy in the face of a constant assumed residual value would inevitably have to seek increased lease rates on that asset to maintain the same return on investment or – alternatively and unpalatably – accept lower returns on the capital invested in their aircraft.

Moving lease rates higher would be difficult in the present environment, given the strong competition among lessors to place a number of different aircraft types. As lease rates are largely set by the demand-side market (lessees) rather than the supply side (lessors), that would put one company at a disadvantage to those that have more liberal policies. Even over the longer term, it is hard to see that situation changing.

Overall, Korn's calls for shorter assumptions on useful economic life and lower residuals certainly have merit. However, unless the industry moves together to a new standard, change appears unlikely.

Source: Cirium Dashboard