ATR and Bombardier enjoy a renaissance of their propeller-driven airliners as demand for small jets collapses

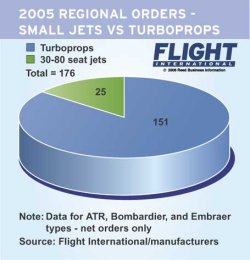

There were two revivals in the regional sector last year, as the resurgence of turboprop sales gave Europe’s sole remaining regional airliner manufacturer ATR its healthiest orderbook for more than a decade. But overall, the regional industry suffered declines in orders and output.

|

|

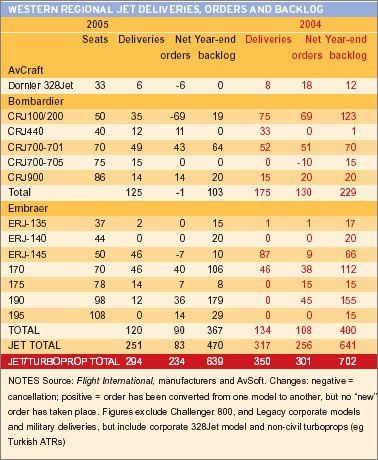

The regional jet net order tally was dramatically reduced as a result of the large-scale order cancellations for Bombardier’s 50-seat CRJ200, which ended 2005 with 69 fewer orders than at the start of the year. Embraer’s 37- to 50-seat ERJ family also suffered, with its orderbook declining by seven during the year, so it is no surprise that production of the CRJ200 is about to be suspended while output of the ERJ is to be significantly curtailed.

Overall, deliveries and orders for ATR, Bombardier and Embraer fell 15% last year to 288 and 240 aircraft respectively (excluding the six Dornier 328Jets delivered by the now defunct AvCraft, which took orders for four aircraft, but suffered 10 cancellations).

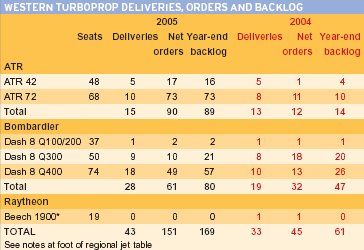

ATR’s 90 net orders (including 10 ATR 72s for the Turkish military) ranks it equal with Embraer, and there was no disguising the Alenia Aeronautica/EADS joint venture’s joy last week in Paris when it announced its 2005 performance. ATR also shaded its transatlantic turboprop rival Bombardier, which mustered 61 Q Series orders.

“This was our best performance since 1989,” says ATR chief executive Filippo Bagnato. “I am convinced last year’s turboprop sales were not a peak. I believe 2005 was the beginning of a cycle.”

Pointing to the industry’s 8% growth last year, Bagnato says that growth in the 2006-9 period is forecast to continue at 5.6-5.7%. He adds that regions such as China and India will offer huge potential for sales of new and used turboprops as deregulation takes hold and stimulates growth. It is not surprising that Bagnato points to India for growth opportunities, given that orders from two of the country’s airlines – Air Deccan and Kingfisher – accounted for more than half of the 90 orders ATR secured last year.

© ATR |

Air Deccan was one of the two Indian airlines that helped bring about the ATR's |

Bagnato says that rising fuel prices have prompted the demise of demand for the small regional jet and the resurgence of the turboprop: “Bombardier and Embraer have virtually ceased 50-seat jet production, leaving the 30- to 70-seat band to the turboprops.”

|

|

As demand shifts from small jets, Bombardier has benefited from its strategy of keeping a foot in both camps with orders for 61 Q Series turboprops providing an effective counterbalance to the raft of CRJ200 cancellations. The result is that the manufacturer’s total 2005 net orders amounted to 60 aircraft (compared with 162 in 2004), as net orders for its regional jets ended the year in deficit (minus one net orders). The good news is that Bombardier nevertheless accumulated a healthy intake of orders for its larger CRJ700/900 family, which lessened the impact of the CRJ200 cancellations.

Embraer’s small regional jets have also suffered, but this has been offset by sales of the large E-jet models, for which Embraer secured just under 100 orders for the second year running to give it a net tally of 90 aircraft. Overall, Embraer’s orders fell by 18 units compared with 2004.

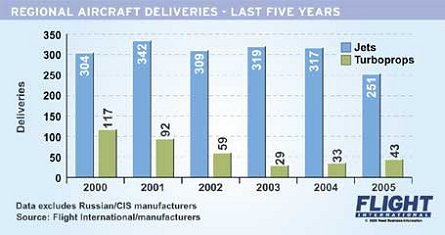

The changing fortunes in orders were also reflected to a lesser extent in output, as deliveries of turboprops rose by 30% to 43 aircraft and regional jets fell by 20% to 251 units.

Bombardier remains the most prolific regional producer, delivering 186 CRJs and Q Series aircraft. However, while Q Series deliveries increased by almost 50% to 28 aircraft, overall its output declined by a fifth due to the fall in CRJ200/440 shipments. Although the shift in demand to larger regional jets helped to partially offset this decline, overall CRJ deliveries fell by 50 units to 125 aircraft.

Embraer also saw its small-jet shipments decline by almost half, to 46 aircraft. However, the expanding production of the new E-Jet family saw output of these models increase by a similar magnitude, to 72 aircraft – deliveries began last year of two new variants. The company nevertheless suffered a 10% overall decline in deliveries. The Brazilian manufacturer says output will remain flat this year and will rise slightly in 2007.

ATR shipments rose slightly from 13 in 2004 to 15 last year, but output is set to rise dramatically following the surge in sales. The company says that 25 aircraft will be handed over this year and output will increase to 40 a year in 2007 and 2008.

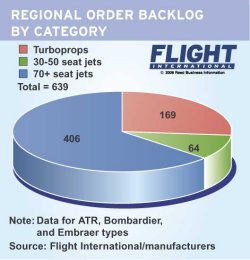

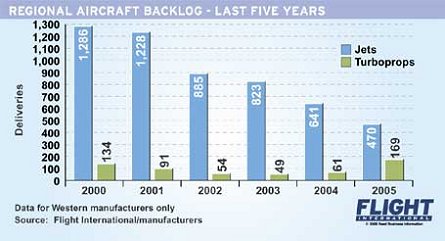

The regional backlog has declined by almost 10% over the past 12 months, to 639 aircraft, which is its lowest this decade. But fortunes are mixed as the turboprop backlog is back at 1990s levels, while jet backlog slumped by a quarter. Turboprop market share has risen to over 25% – its biggest chunk of the pie for a decade.

Meanwhile, the fledgling regional jet manufacturing industry in Russia, the CIS and China continues to strengthen. The Antonov An-148 70-seater is well into its flight-test programme and landed its first firm orders last year, while engineering efforts to turn the Sukhoi Russian Regional Jet (RRJ) and China’s ARJ21 large regional jets from paper projects to reality are gathering momentum.

The RRJ secured an important seal of approval last year when Aeroflot Russian Airlines signed for 30 aircraft for delivery from November 2008. This pushed its orderbook to 100 aircraft.

There are already a number of major international suppliers on board the 95-seat regional jet, which is powered by a new engine being developed by Franco-Russian joint venture PowerJet (which comprises Snecma and NPO Saturn). Italy’s Finmeccanica is also poised to decide whether to take a 25% stake in the programme for its airframe division Alenia Aeronautica.

Source: Flight International