After the fuel volatility and credit crisis that ravaged airlines in 2008, last year was dominated by the economic crisis, which crippled demand. The industry may not have been splattered in quite so much red ink as when fuel hedging contracts went awry, but revenues took an unprecedented hit. Even for this punch drunk industry, the revenue falls evident at the world's biggest carriers in the 2009 Airline Business Top 150 world airlines (for more on how to get these and other Airline Business rankings go to flightglobal.com/datasets) is startling. Overall revenues for the Top 150 airlines slumped 11% to just over $500 billion. This is the first time in a decade, revenues seriously contracted.

|

|---|

Has the industry learnt its lessons from the crisis? (pic credit: Rex Features) |

That profits did not go the same way owes much to the capacity cuts and efficiencies implemented across the sector. Net losses among the Top 150, at $7.8 billion, were less then a quarter of that seen in 2008. At an operating level, the Top 150 airlines even managed to record a small operating profit.

|

|---|

This was aided by the pace of the economic recovery. IATA sprung a surprise in March by cutting its industry loss forecast off the back of the stronger than expected last quarter in 2009. Three months later, it was predicting the first industry profit for three years in 2010. While the recovery is far from balanced - Europe is expected to lose money again while all other regions return to profit - traffic, revenues and yields are all on the up. After global losses in 2009, IATA now expects an industry profit of $2.5 billion this year. It has forecast a $4 billion swing in North American airline profits in the last three months alone.

"The airline recovery, if you want to call it that, has outpaced that of the economy," notes Tim Claydon, commercial adviser to several airlines including AirAsia. "I do think the recovery has been a relatively pleasant surprise for a lot of airline CEOs around the world and it has them looking forward more to where they go from here, rather than addressing the fundamental issues."

|

|---|

See our graphic representation of the 2009 rankings here |

The potential danger is that the economic recovery has taken hold so quickly, that structural changes at both industry and airline level may not have been implemented. This could encourage some airlines or governments to put tough decisions on hold or make it harder to gain support for them.

SNAPSHOT |

|---|

$510bn |

Revenues fell 11% among the top 150 airlines in 2009 |

$197m |

2009 operating profit for the top 150 airlines. In 2008 the operating loss was $15.1bn |

$1.7bn |

Net profit for low-cost carriers in Top 150 compared with a $9.7bn loss for network airlines |

$28.9bn |

Merger partners United and Continental would be the third largest carrier by revenues. BA and Iberia would be 6th largest, with $18.9 billion in revenues |

But ultimately the Airbus and Boeing order books remain full with new deliveries, and Claydon notes aircraft parked during the crisis could easily return. "After 9/11 and fuel, people knew those parked aircraft would never go back into commercial service. But where you have got, say A320s parked there, those aircraft can very easily be flown back in." IATA reports 100 aircraft were taken out of storage in May and 93 new aircraft were delivered. It says this, combined with aircraft utilisation rates still below pre-recession levels, make matching capacity to demand "increasingly challenging" in the coming months.

No Cull In Carriers

Neither have the number of players in the industry been culled to the extent people had feared, or in some cases, hoped for. There has been consolidation, airline failures and limited new entrants. But after a flurry of airline collapses during 2008 and early 2009, few players have since been lost. "The crisis teaches us, yet again, that the airline industry is a lot easier to get into than it is to get out of," says Cathay Pacific chief executive Tony Tyler. "Despite the crisis, not many airlines have failed. At the end of the crisis, we are just as oversupplied as we were going into it. That is always the case and will continue to be until governments learn that airlines are companies just like any other."

Consolidation continues, evidenced by the planned tie-up of Greek carriers Aegean and Olympic Air to help counter economic woes and the strategic merger between US majors United and Continental. But consolidation takes time and the focus of many is on integrating what is already on the books and expanding partnerships and joint ventures.

Throughout the crisis, the presence and influence of low-cost carriers has continued to expand, notably in the newer markets of Asia and the Middle East. Low-cost carriers now account for nearly 10% of the Top 150 airlines revenues, and outstripped their network peers in profitability during the crisis. It was the most profitable of all sectors in 2009, posting a collective net profit of $1.7 billion compared with a network carriers' net loss of almost $10 billion in the Top 150 ranking.

So, perhaps unsurprisingly, low-cost carriers believe having a cost base which enables them to stimulate demand through low fares is one of the key lessons of the crisis. "I think we have learnt, even during difficult times, there is latent demand for travel," says Air-Asia X chief executive Azran Osman-Rani. "You just have to be more aggressive in pricing structure."

The Middle Seat Airline

While there has been a blurring of the lines between full-service and low-cost carriers in short-haul markets, Azran - pointing to how other industries have evolved - believes airline will become more focused. "[It will rest on] whether you command a brand premium and people will pay a premium for your service, or if you are a mass operator and you live on volumes. The problem comes when you are stuck in the middle, where you don't have the brand premium or the cost structure."

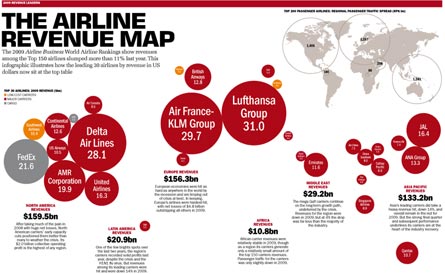

TOP TEN AIRLINE GROUPS BY REVENUE (2009) |

|---|

Rank Airline 2009 Revenues Change in $ |

1 Lufthansa Group $31.0bn -15.0% |

2 Air France-KLM $29.7bn -14.7 |

3 Delta Air Lines $28.1bn 23.6 |

4 Fedex $21.6bn -3.6% |

5 AMR Corp $19.9bn -16.2% |

6 Japan Airlines* $16.4bn -19.5% |

7 United Airlines $16.4bn -19.1% |

8 ANA Group $13.2bn -4.3% |

9 British Airways $12.8bn -14.8% |

10 Continental Airlines $12.6bn -17.4% |

Notes: Based on latest full year figures except Japan Airline where financial year figures unavailable. Figures used are based on combination of last four available quarters running to Dec 2009. For how to get the full Top 150 and analysis, go to flightglobal.com/datasets |

"The main efforts have to be made in the creation of a new high-level product for the business class clientele. It is interesting to see that the Gulf carriers and in particular Emirates, which has the best service, have not suffered from this crisis and they continue to make profits," he says.

Andrew Herdman, director general of the Association of Asia Pacific Airlines acknowledges aviation remains a highly competitive industry, facing constant challenges. "Air fares do not keep pace with general price inflation, so the industry has to maintain a constant focus on productivity improvements, even as we meet growth in demand. The industry will continue to evolve," he says. "The dynamics of market competition and rivalry amongst competing business models will continue to drive change and further innovation."

Asia Leading The Way

Airline fates are entwined with economic fortunes, and the improved outlook for the industry reflects the brighter, if fragile, economic performance seen since the second half of last year. While Latin America has generally been the region to come through the crisis most unscathed, it is Asia that is at the heart of the recovery.

"The rebound marks a welcome, and surprisingly strong, V-shaped recovery following the sharp slump in demand experienced during the world recession," says Herdman. "The outlook for the coming months remains broadly positive, supported by Asia's buoyant economic growth, although some concerns remain over regional imbalances, as well as oil and currency volatility."

Herdman notes Asian carriers learnt from past experience, by making relatively few staff retrenchments during the crisis. This positioned them to quickly bounce back when demand returned. "Even during the recession, the underlying demand for travel and tourism was always evident, though businesses and consumers were understandably cautious. Longer term, the aviation industry is projected to continue growing at around 5% annually over the next two decades, with slightly faster growth in Asia."

Cathay's Tyler agrees: "We have learned the same lessons as we learned in the past. Don't panic when things get bad. We are based in Asia, which is a success story. Things come back here quicker than anywhere else. Secondly, as much as possible, keep the team together. Do sensible things to preserve cash, delay aircraft, stop building that cargo terminal, restructure the balance sheet and the earlier you get onto it, the better."

One of the most obvious challenges to future airline profitability is continued fuel price volatility. The scars remain from an oil price in excess of $140 per barrel two years ago. Steady rises saw it reach nearly $90 per barrel in April. While the price has since fallen again, it served as a reminder of the damage high fuel costs can cause.

But while fuel crops up in almost every airline executive's list of concerns, there is a sense the sector may be better placed to deal with such a volatility again - even if it is only because they have been through the experience before and it is a problem all airlines will have to deal with.

Fuelling Concerns

"Fuel, we've been down that road before," says Claydon. "You can ask three people about fuel and get three different answers. But I do believe there is going to be a much more systemic hedging policy going forward. It is always something that is going to be a concern, but I certainly feel the finance departments at airlines have a much better view on how to handle fuel fluctuations."

Airlines will likely use a mix of tools for mitigating the fuel impact; surcharges at the consumer end, hedges from the financial side and utilising more fuel efficient equipment from the operational standpoint. "[Hedging] doesn't alter the fact that costs are going up [if the fuel price rises]. It merely postpones it," says Malaysia Airlines chief executive Azmil Zahruddin. He notes that even if you mitigate your costs by using more fuel efficient aircraft - Malaysia Airlines is itself embarking on a major fleet renewal - ultimately if fuel prices go up, the extra costs will eventually have to be passed to the consumer. "At the end of the day, you still burn fuel," he says.

Ironically, airlines could still face fresh cost pressure, even if fuel prices stay low and the recovery proves rapid and sustainable. A decade largely of toil has seen airlines regularly knocking on labour's door looking for concessions. Any improved outlook seems likely to have labour in the mood to win back lost ground. "There are expectations, and the biggest driver of that would be the fuel price," explains Marty Kuehne, managing director for human capital at Seabury Group. "It would be very difficult to negotiate with prices at $73 per barrel, if your biggest cost is about half what it was 18 months ago. In the last 10 years or so, there has been so much on concessions and implemented [during formal restructuring], it will be very difficult if fuel prices stay low or the economy and revenues pick up."

Again there is no one-size fits all, with different dynamics across the regions. "Europe, and to some extent the Middle East, is in the process of experiencing what the US industry went through in the last couple of years," observes Kuehne. He points to a number of elements US carriers went through in their labour strategies; reducing the fixed costs elements attached to labour - such as restructuring pensions - increased outsourcing of labour in areas like ground services; and descaling, by which different conditions apply to new staff from existing staff.

In the US sector, where labour has already negotiated concessions and in some cases had more implemented through the bankruptcy courts, attentions are turning to a new stage in the process. Revenues are already improving and the appetite to win back lost concessions is growing. "Clearly in the US there is a driver to regain what they lost in the bad times. But there is a lot of flying capacity that was pulled down. I think its still going to be a difficult environment," says Kuehne.

Managing these expectations and labour relations in general will be a key challenge for airline management, particularly for airlines already seeing a fast improved financial position. "The really difficult thing about collective labour bargaining is your most irrational competitor creates the market. All it takes is one carrier to take a view on the outlook and revenues and decide we are going to be willing to pay x amount," notes Kuehne. "I think there is always an opportunity to work together. But management always tends to focus on what to pay, and unions focus on the competitive market position. The bridge is to create enough of a transparent model that they can make those decisions."

Source: Airline Business