Rolls-Royce will make the news later this month when Airbus delivers the first A350 to launch customer Qatar Airways – powered, as all A350s will be, by the UK engine maker’s Trent XWB. But even on the eve of achieving this milestone, the company made the financial news last week with a call for its breakup.

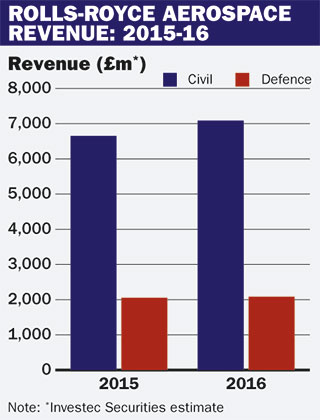

According to London investment bank Investec Securities, R-R is an underperformer that has been following a misguided strategy to become a diversified industrial group – when it should, perhaps, be focusing on its core business of gas turbine engines for civil aerospace. This accounted for 42% of 2013 group sales, and is expected to show good growth over the next couple years (see chart).

Unsurprisingly, powerplants for military applications don’t show such growth prospects, but sales represented 17% of group revenue in 2013 and Investec recognises “tangible benefits and synergies” from running the civil and defence aerospace businesses side-by-side. However, it claims that investors “continue to doubt the rationale of combining this grouping with other industrial assets”. Those assets – which accounted for half of 2013 revenue – include land and marine gas turbines, nuclear power systems, design of ships and other marine equipment and marine piston engines.

What Investec wants from chief executive John Rishton and the board of directors is a serious review of a strategy that has, over the past several years, seen Rolls-Royce spend some €4 billion ($4.9 billion) to first form a marine diesels joint venture with Daimler and then take complete ownership of the former Tognum business, now known as Rolls-Royce Power Systems. Concern over this strategy was elevated in October 2014, when R-R issued a profits warning on the back of deteriorating economic conditions hitting power systems, nuclear and marine – along with the continuing slump in defence spending.

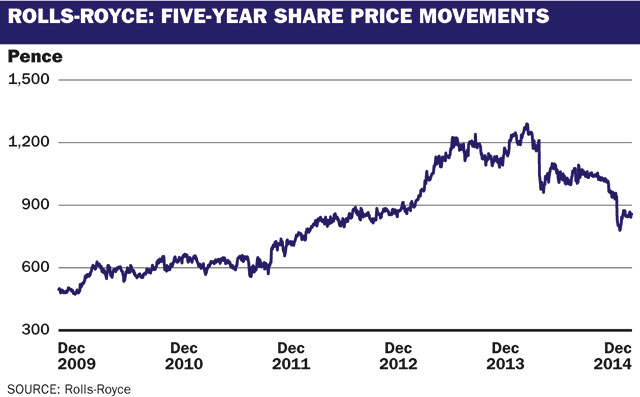

Ideally, says Investec, that review will lead to a breakup of the company – either a straight split into two companies, along the lines of the existing Aerospace and Land & Sea divisions, or a sell-off of non-aerospace assets, which could return some £6bn to shareholders. Realistically, the bank expects the board to decide to maintain the “status quo”, a strategy that would leave R-R looking like United Technologies (UTC), GE or Honeywell, rather than to create a pure-play aerospace firm. But even with no change, the discipline of a thorough strategy review would, it reckons, at least help the board to better communicate its ambitions and regain collapsing shareholder confidence (see chart).

One explanation for Investec’s proposal is that, like many investors, it does not like conglomerates. Managements typically justify diversification strategies as means to protect their firms from downturns by building a counter-cyclical portfolio. lnvestors, however, generally feel that portfolio building is their job – and that managements should focus on their strengths and give investors clean options unless there are very clear synergies between divisions. In the case of Rolls-Royce, this means 'don’t make me buy marine pistons and nuclear submarines when what I want is to put my money into aerospace gas turbines.'

Not all investors agree that R-R aerospace suffers, however tenuous its links to the rest of the group. But Investec’s analysis of its situation draws useful attention to the challenges facing the aero engines part of the company. As Investec’s Rami Myerson sees it, in the short term R-R has got to match, with its Trent XWB, Airbus’s A350 production ramp up. And, he adds, the Trent 1000 option for Boeing’s 787 remains a priority while the company has committed to develop a Trent 7000 to power Airbus’s re-engined A330neo, set to enter service in 2017.

In the longer term, R-R needs a plan to return to the narrowbody airliner market, which it exited when it sold its stake in the International Aero Engines consortium to Pratt & Whitney in 2013. Myerson observes, however, that such an engine could be a very expensive project, potentially costing more than the old $1 billion per engine rule of thumb. Business jets are also a segment where R-R has been losing ground recently and may need to invest to regain market share.

There is another consideration to splitting the company into Aerospace and Land & Sea companies. With a separate arrangement for the nuclear submarine business, the UK government’s golden share would become irrelevant, raising the prospect of foreign takeover. London has tended to be sanguine about “losing” industrial crown jewels in the past, so such an outcome isn’t unthinkable.

For its part, R-R describes itself not as a diversified industrial but as a "strong high-tech engineering company specialising in engine technologies and related high-tech areas". And, it says, synergies are strong across the group - for example in materials technologies that have wide applicability across both divisions.

Richard Evans, formerly with Rolls-Royce and now a consultant with Flightglobal’s consultancy arm Ascend, sees in R-R an essentially strong company that is technologically more or less on a par with its rivals. R-R, he notes, is stronger today than it was a year ago because it has the A330neo-Trent 7000 job on its plate – but it is weaker than five years ago, when its involvement in IAE and its V2500 narrowbody engine gave it a wider portfolio.

Few would argue with Evans, who sees the priorities now as cutting costs and improving profits. Rishton said as much in November when he announced 2,600 jobs cuts, mostly in aerospace, “as part of an intensified programme to improve operational efficiency and cut costs”.

Source: FlightGlobal.com