IATA’s latest industry outlook underlines the improving fortunes of airlines in mature markets as it sees North American carriers as not just the most profitable but also the only region where profits expectations have improved.

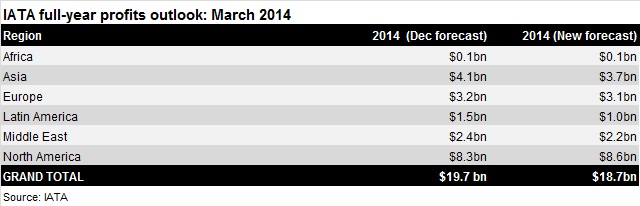

The association’s latest quarterly financial outlook released today, forecasts North American carrier profits of $8.6 billion for this year. This is $0.3 billion higher than it was projecting for 2014 three months ago in its December forecast.

This improvement comes despite IATA having tempered its expectations that fuel prices might ease slightly in 2014, a pressure that prompted IATA to cut profit forecasts for most other regions and for the industry as a whole by $1 billion to $18.7 billion.

“The success of the North American industry demonstrates clearly the benefits of consolidation and joint ventures,” says IATA director general Tony Tyler, adding this has not come at a cost to the customer. “There are still four very large national airlines that fly almost everywhere. While they have strengthened their financial position, there is still a significant choice available for consumers.”

North American carriers are expected to account for nearly half the total industry profits of $18.7 billion in 2014. Profits for carriers from another mature region, Europe, have been scaled back by $100 million. But the $3.1 billion return European carriers will make is still $2 billion more than in 2013.

It means European and North American operators combined will generate $11.7 billion of total industry profits of $18.7 billion in 2014. Compare this with the $4.5 billion losses these carriers incurred as they drove an industry loss of $5.6 billion in 2010, and the change in fortunes of airlines in these two markets is clear.

Tyler notes it is now the developed economies that are leading passenger growth. “And we see many developing markets – India, Brazil, etc – showing slower growth trends,” he adds. “Growth in emerging markets generates proportionately larger traffic flows than in mature markets. So we have had a slight downward revision in expected passenger traffic growth rates from 6.0% to 5.8%.”

IATA still expect Asia-Pacific carriers to be the second-most profitable region, generating profits of $3.7 billion. However, this is $400 million lower than the figure it expected three months ago and only $700 million higher than the 2013 figure.

“The improvement in cargo prospects is helping,” says Tyler. “But this is being offset by slower growth as countries like India and Indonesia cope with the impact of the turmoil in foreign exchange markets.

“The Asia-Pacific carriers have suffered disproportionately by the weakness in the air cargo market, which has flat-lined since 2010,” says Tyler of the changing fortunes for the region. “We have also had economic growth in Asia less robust than in previous years, whereas in Europe economic growth has been more robust than in previous years.”

IATA has trimmed its profit forecast for Middle East and Latin American carriers to $2.2 billion and $1 billion respectively.

Tyler points to continued strong expansion of market share among the Gulf carriers and strong cargo performance – particularly on routes connecting Africa and Asia. The higher fuel burden, though, means the region’s profitability has been scaled back $200 million.

IATA has taken $500 million off its expectations for Latin American airline profits this year. “The weak economic performances of Brazil and Argentina are dampening prospects,” says Tyler.

Prrofit expectations for Africa are unchanged for the year at $100 million, which marks an improvement on the $100 million loss incurred in 2013. “We are seeing improving economic performance in the region,” says IATA chief economist Brian Pearce. “The African market is quite mixed. There are some successful airlines and we are seeing some structural improvements.”

While the passenger traffic outlook for 2014 has weakened slightly, the air freight picture is finally improving. “Instead of the previously projected 2.1% growth, it now appears that air cargo is headed for 4.0% growth in 2014,” says IATA. “And the yield decline will be moderated from the previously forecast 2.1% fall to a decline of 1.5%. Trading conditions remain challenging, but positive macroeconomic trends are providing a much-needed boost.”

The cargo picture provides a lift for airline fortunes, but it is the higher fuel bill that has prompted the lower of profit expectations for the year ahead.

“The [forward oil price prediction] has shifted up several dollars in the last month, largely because of the situation in Ukraine,” says Pearce. IATA had hoped for a slight reduction in fuel prices as a result of increased supply in North America. “That has been wiped out by the uncertainty, so we now expect it to stay roughly where it was at $108 per barrel of crude oil.”

The uncertainty around the political situation in Ukraine is one of the possible risks to airline profits that IATA identifies. “It is very difficult to anticipate how these geopolitical risks can develop,” says Pearce, pointing to the impact on energy prices and travel demand. “[But] the only change [we have made] is to look at how the current uncertainty might reflect in higher energy prices.”

IATA also points to the possible negative impact on traffic of action in several markets that might serve to slow economic growth. “Many countries – including Turkey, India, Indonesia and South Africa – have tightened monetary policy in order to protect exchange rates, slowing economic growth,” says Tyler. “And we see this trend continuing.”

Despite these risks, the projected $18.7 billion industry profit would be nearly $6 billion up on the 2013 figure and would top the previous high of $17.5 billion recorded in 2010 (an annual figure restated from $19.2 billion following the restatement of ICAO data).

Pearce also takes heart from the continued match in supply and demand. “In the past it has been a real problem appropriately matching capacity with demand,” he says. “[In recent years] airlines have been much better at adding appropriate capacity with the market demands.”

He notes that while passenger capacity was increased further in January, this was more than matched by increased traffic. “We are seeing an acceleration of capacity being added in 2014, but at the moment that seems to be matched by the demand for air travel. So at the moment it looks like quite a sensible addition.”

Source: Cirium Dashboard