Leisure carriers in Europe have not been short of challenges over the past 12 months. Already adjusting to falls in demand to North African destinations, further tourism hotspots have been hit by damaging geopolitical events. On top of that, the Brussels and Istanbul airport terror attacks highlighted the vulnerability of travel infrastructure to already-wary customers.

Operators could at least reassure themselves that people would still want to go on holiday; as some destinations lose popularity, others pick up the slack. That has happened to an extent, with western Mediterranean resorts in particular seeing rising demand, but the money does not necessarily flow towards these "safer" destinations in equal measure. And with fewer places to choose from, competition hots up on the routes that remain – not just from dedicated leisure carriers.

The consequent danger of overcapacity and yield pressure for Europe's leisure carriers could be exacerbated in months to come by other developments: economic indicators have softened and the region has been rocked by the UK's vote to leave the EU, both factors potentially hitting demand for leisure travel.

Several carriers are also expecting new aircraft, often ordered at a time when the market looked very different. UK leisure operator Thomson Airways, for example, has 50 aircraft on order against a current fleet of 63, Flight Fleets Analyzer shows.

"The switch [to leisure destinations considered safer] has been compounded by the continued rapid fleet growth of carriers with more focus on leisure routes," says analyst Carl Denton of Sven Carlson Aviation Consulting. "Route planning has been focused on the thicker and what are perceived to be the commercially safer routes, but this is resulting in pressure on destination bed stock and multiple carriers competing on the same or similar routes."

The mixed performances that emerged during the recent earnings season demonstrated the impact of these factors. UK-based package holiday company Thomas Cook, for example, saw operating profit fall to €2 million for the second quarter of 2016, down from €28 million in same period of 2015. It cited overcapacity and increased pricing pressure "due to intense competition in the short- and medium-haul market". Even as some leisure operators continued to see modest profit growth, the outlook was cloudy.

Lufthansa-Turkish Airlines joint venture SunExpress stands out as a leisure carrier more exposed than most to recent events in the region. It has a big presence in two markets where appetite for leisure travel has been significantly dented: Turkey and Egypt.

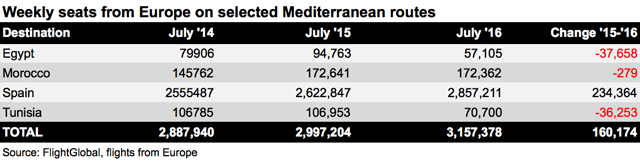

Turkey had long been an attractive destination for European holidaymakers. But the combination of June's terror attack at Istanbul Ataturk airport, followed the attempted coup in mid-July and its tempestuous aftermath, has led to a drop-off in leisure demand. Turkey's ministry of culture and tourism says that in July foreign visitor numbers were down 37% year-on-year, from 5.5 million to 3.5 million.

In Egypt, leisure-traveller confidence in security procedures is still low following the October 2015 crash of a MetroJet A321 in Sinai after departure from Sharm El-Sheikh, to which many carriers are still reluctant to fly. Russia has initiated a total suspension of flights to Egypt. Political unrest in the North African country has also put a cap on demand. The most recent statistics from the World Travel & Tourism Council show Egypt's tourist visitor numbers down 46% year-on-year for the first two months of 2016.

The answer for SunExpress has not been to abandon its core strategy, but to look elsewhere for growth opportunities. "Our clear strategy is to stay with our high Turkey engagement since Turkey is our home, and in parallel develop new flight opportunities to the Canary Islands, Bulgaria and other southern destinations," it says.

Despite these efforts, Lufthansa announced in August that SunExpress capacity was being redirected to the German group's low-cost outfit Eurowings. Lufthansa chief executive Carsten Spohr cited "large declines" in SunExpress's traditional markets as the decision was disclosed.

"Airlines have had to react quickly to the reduced demand in these markets and this has led to some suboptimal reallocation of capacity," says analyst John Strickland of JLS Consulting.

TURKEY FACTOR

Meanwhile, pan-European travel giant TUI, which counts Thomson Airways among its subsidiaries, has acknowledged the challenges it faces but retains a confident outlook. Crucially, it lacks a big presence in Turkish markets.

David Burling, managing director of the northern region on the executive board of TUI, said at July's Farnborough air show that short-haul Mediterranean routes were the main focus for the group, and that recent terrorism incidents had shifted traffic elsewhere, rather than removing it completely.

"What we have seen is a move from destinations like Turkey to Spain this summer," Burling says. "But that has been reasonably positive for us.

"I think the TUI Group and the travel industry in general is very adaptable. Flexibility is in our DNA."

Rival holiday group Thomas Cook, the airline operations of which include Germany's biggest leisure carrier Condor, is attempting to prove that flexibility, particularly in light of its significant exposure to Turkish destinations. "We've taken action to further reduce our capacity to Turkey and increased sales of holidays to other areas, including the western Mediterranean and long-haul destinations such as the USA," states chief executive Peter Fankhauser in an August earnings report. "Growth to smaller destinations such as Bulgaria and Cuba is also strong."

For carriers such as SunExpress and Thomas Cook, it might not be long before more destination options are on the table, potentially offering yield and capacity relief. Even a possible return to North African routes – abandoned after geopolitical unrest and terror events – cannot be ruled out in the medium term.

"There are positive noises regarding the reopening of Sharm el-Sheikh," says Denton. "And with increasing pressure on costs and yield, the significant value for money that North Africa and Turkey could offer with good access to bed stock – compounded by overcapacity and limited bed stock on the higher-volume routes – will increase commercial pressure for the holiday companies to start to switch some capacity back."

Strickland cautiously concurs: "Over time we can expect to see a more considered approach to redeployment but it's difficult to say when the affected markets will recover and to what extent."

Europe's leisure market also knows that the impacts of economic, geopolitical and terror-related factors may take some time to manifest themselves. Leisure markets tend to work in cycles – many people would have booked summer 2016 holidays before events in Turkey and Brussels, and before the Brexit vote, for example. Currency effects are a potentially influential unknown.

"Given the lags in the system, the impact will be delayed," says aviation analyst Chris Tarry of Ctaira, citing the UK's currency weakness following the Brexit vote. "Currency will have an immediate effect on those who have already booked in terms of how far their pound goes when they get there, but this has no real impact as the package has already been sold. The real impact will be on the 'lates' market, where prices will have to fall further to get the deals sold."

LOW-COST COMPETITION

The fight for yield advantage, particularly with capacity being squeezed into fewer destinations by picky customers, is further complicated by competition from low-cost carriers on leisure routes.

Monarch Airlines has seen things from both sides of the fence. The UK carrier jumped ship from charter operations and reinvented itself as a 100% scheduled operator in 2015 – successfully enough to become the subject of speculation about a takeover by EasyJet earlier this year. The idea of EasyJet taking on Monarch – denied by both parties – highlights the blurred lines between leisure and low-cost operators, which increasingly compete on similar terms.

"Controlled product and distribution is increasingly important and you see the LCCs – especially Jet2, Monarch and, to a lesser degree, Norwegian and Ryanair – moving more towards what would traditionally be considered and charter/tour operator model with their own holiday brands and more open to the concept of third-party distribution," says Denton.

But does this threaten the very existence of dedicated leisure carriers in Europe?

"For large leisure groups there is still value in control of seat inventory by owning an in-house carrier, but there are equally cost benefits in tapping into inventory of LCCs as required and thus avoiding cost and reducing risk and exposure to market sensitivities," says Strickland.

Lithuania-based Small Planet Airlines is attempting to prove that small charter operators still have a place, too. The carrier has partnered with TUI and Thomas Cook, operating charter flights for the two tour operators since May this year. Andreas Wobig, chief executive of the carrier's German operations, still sees a role for charter carriers in Europe. "We think that full or partial charter flights – where an aircraft is hired by a tour operator – will continue to exist in future," he said in March.

For now, most of Europe's leisure carriers – chartered, scheduled or hybrid, big or small – will be hoping for two things: a quick return to currently off-limits destinations to alleviate yield pressure, and an economy that avoids storms on the horizon and gives customers the confidence to continue spending money on leisure travel.

Source: Cirium Dashboard