George Dimitroff, head of valuations with Flightglobal advisory service Ascend, looks at how values and lease rates are faring

The airline industry ended 2013 in a good state of health: another year of profits, stronger balance sheets, stable fuel prices and overall optimism. In fact, IATA predicts even higher traffic growth and higher profits for 2014. Combined with a robust and improving global economy, those predictions are very credible.

Yet airline profits are not a new thing: over the last four years airlines have churned out reasonable profits thanks to capacity discipline, while aircraft values still suffered because older equipment was largely unwanted. Shiny new units rolled off the production lines in increasing numbers, and continue to do so – but it finally appears like demand is picking up to a sufficient level to be able to start absorbing some mid-life aircraft and not just the latest production inventory.

With the arrival of a new year, Ascend’s values review board takes these factors into account as we conduct the scheduled market values and lease rates update (most other changes are “non-scheduled” in that they occur as and when we see market changes). The principal driver behind this discipline is the introduction of a new year of build and the consequential impact on other vintages, which are now all a year older.

In a positive move, Ascend has already moved Airbus A320 lease rates modestly upward since the beginning of the year, to reflect firmer pricing on new leases of mid-life aircraft, generally defined as post-2000 vintage. The availability of new single-aisle types from lessors’ speculative orderbooks has more or less dried up for the next couple of years, so if an airline wants to get its hands on one, it has to start looking at some mid-life examples that have come off their first lease. This dynamic has already started to assert itself, not just on A320s but also on the smaller A319. The improvements so far have been very modest, but we can say confidently that the worst is behind us.

As most five- to seven-year leases signed pre-2008 have now expired and lease terms have become longer, there will also be a reduced number of lease expiries over the next couple of years, which should positively impact lease rates further.

Ascend Online Fleets data shows that the number of used aircraft sales picked up in 2013 for aircraft aged under five years or five to 10 years. Sales of aircraft in the 10 to 15 year age bracket could be next (they were flat in 2013), although this hinges on several prerequisites. Historically, an increase in trading eventually results in improved values. There is still a lot of potential obstacles, a lot that could go wrong, but overall, leading indicators point towards an improvement in values and lease rates for good-quality mid-life aircraft.

One of the drivers behind this is the increase in investors seeking to enter the mid-life aircraft space over the past year. Yields are inevitably higher when financing mid-life aircraft, reflecting the higher risks that investors have to take, but with more buyers competing in the space and competing against each other for the same acquisition opportunities, we may see aircraft values pushed up a little.

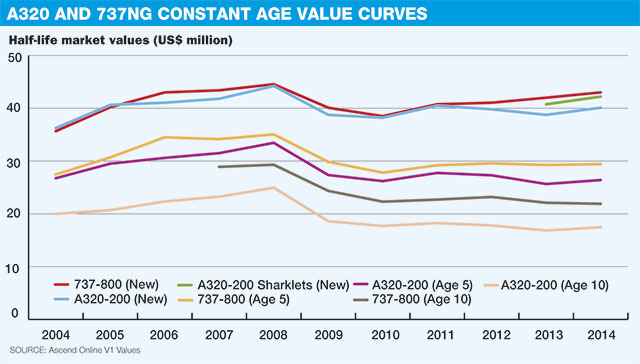

The chart below shows constant-age market-value curves for new, five- and 10-year-old A320s and Boeing 737-800s, the two most liquid types in the single-aisle market. New values show the most distinct improvement, with sharkletted A320s now close to the market leading 737-800. Five-year-old A320s also show some improvement, while 737-800s are more stable because their values recovered earlier, back in 2010. But most interestingly, the line for the 10-year-old A320 also shows a gentle, albeit small, improvement.

There continues to be order upsizing to the A321 and 737-900ER and their value movements were in line with expected annual depreciation. For the smaller A319 and 737-700 there has been some improvement in market perception, and depreciation was relatively small in January, after values took several hits in 2013.

The older-generation single-aisle types continue to be phased out and their markets focused on cash sales in emerging markets. For example, 737-300/400 market values fell 10-18% but this further boosts freighter conversion opportunities. Boeing MD-80 values are already at low levels but fell further, by up to 20% for some younger vintages.

On the twin-aisle front, the market for new production types has been improving consistently. The market’s enthusiasm is more focused on newer models such as the Boeing 787 and Airbus A350, with sales and leasebacks of the 787-9 and A350-900 eagerly anticipated. There is still plenty of activity involving new 777-300ERs and A330s, and newer values have continued to go up in early 2014 as a result mostly of new price escalation (driven by longer lead-times), with used values falling as expected, by around 6-8%.

Previous-generation models continue to fall in value, with Airbus A340-300s and low-weight (pre-1999) A330-300s declining around 17-19%. Values of older high-gross-weight A330-300s will probably remain fairly stable this year, while A330-200s are still under some pressure.

The Boeing 767-300ER and 777-200ER are starting to increase in availability, and their values decreased 7-10%. Values of the latter may decline further if we see more part-outs, although the part-out companies have expressed that they are staying away from Rolls-Royce Trent 800-powered examples.

The Boeing 747 is now pretty much a part-out story regardless of age, and values fell 25% at the start of 2014. The cargo market also continues to be marked by significant long-haul overcapacity and 747-400 Freighter values fell 10-15%, the higher end reflecting converted examples.

The 50-seater jets remain under pressure with US fleet phase-outs and have experienced value reductions of 7-20% in the last four months. There is a more positive picture for the larger regional jets, with the Embraer 175 and 190 in line with the expected annual values depreciation.

The turboprops continue to shine brightly, as their economics on the shortest-haul routes are unrivalled. Values have either remained stable (Saab 340), moved in line with expectations (ATR 72) or even increased (smaller QSeries late last year).

Overall, Ascend sees 2014 as a year in which we will see continued recovery, particularly trickling down to mid-life aircraft. We expect that lease rates will see a more pronounced recovery in the short to medium term than values, as airlines and investors hesitate to take on longer-term residual value risk but are willing to pay extra to get capacity in the near term in order to meet rising traffic demands. Values of mid-life aircraft have potential to improve but this would be driven more by competing investors entering the space rather than by demand from airlines to purchase such aircraft.

Source: Cirium Dashboard