Other simulator manufacturers include Lockheed Martin Commercial Flight Training (LMCFT), which acquired Sim-Industries in 2011, and Mechtronix.

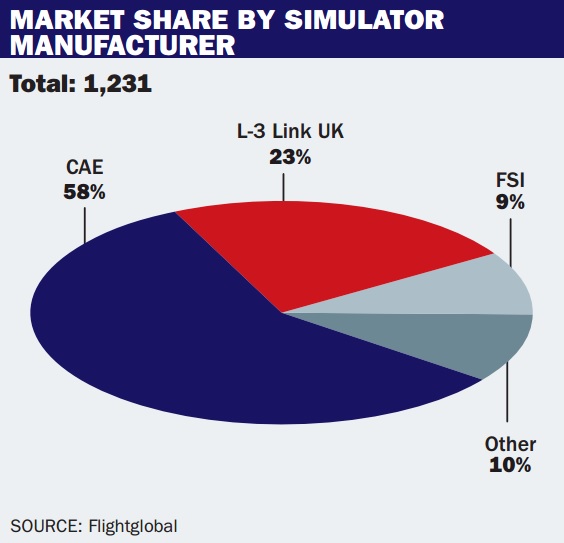

Flightglobal’s latest figures record a total of 1,231 commercial simulators in use in the industry. A total of 34% of these devices are based in North America (the USA accounting for 30% of the world) while Europe and Asia-Pacific have 27% and 26% of the share respectively. Looking at the leading countries, China comes in second after the USA with a 9% share for the 107 simulators based there. The UK and France are the most popular locations for Europe where a combined number of 134 simulators are based.

While three manufacturers are pre-eminent on the equipment side, the marketplace in terms of operators is much more fragmented. According to proprietary figures, CAE is again the biggest individual player with a 14% share of the training market. The company operates training facilities around the globe and owns close to 170 airliner devices based across 26 countries. FlightSafety International, American Airlines and Boeing Flight Services follow with shares of 6%, 5% and 4% respectively. Operators with smaller shares than that make up the remaining 71% of the market.

When it comes to aircraft types, the Airbus A320 and Boeing 737 families – NG and classic variants combined – dominate with 21% and 18% of the market share respectively. Simulators for the A330/A340, 777 and 747 widebodies have shares of 9%, 6% and 5% of the overall marketplace. Boeing represents 46% of the airliners simulated while Airbus totals 33%. Embraer, Bombardier and ATR account for 7%, 6% and 3% of commercial aircraft simulated while the 5% represents other aircraft manufacturers.