The launch by GECAS and Israel Aerospace Industries of a cargo conversion programme for the Boeing 777-300ER provides a potentially sizeable secondary market opportunity for the large fleet currently operating in the passenger sector.

The launch by GECAS and Israel Aerospace Industries of a cargo conversion programme for the Boeing 777-300ER provides a potentially sizeable secondary market opportunity for the large fleet currently operating in the passenger sector.

GECAS

GECAS and IAI unveiled the conversion programme on 16 October, with the leasing giant placing a launch order for 15 firm conversions with 15 options. It is also co-investor of the programme. Designated 777-300ER Special Freighter (SF), this is the first after-market cargo modification launched for the 777 family, with certification and service-entry scheduled for late 2022.

GE Aviation is sole powerplant supplier on the -300ER and GECAS says the engine maker is supporting the conversion programme. The two companies are working together to support packages for the -300ER’s GE90-115B specifically for the freight sector.

“We’re dubbing the -300ERSF the ‘Big Twin’ as it’s 10 pallet-positions larger than the [777-200LRF] factory freighter,” says Richard Greener, senior vice-president and manager of GECAS’s cargo aircraft group.

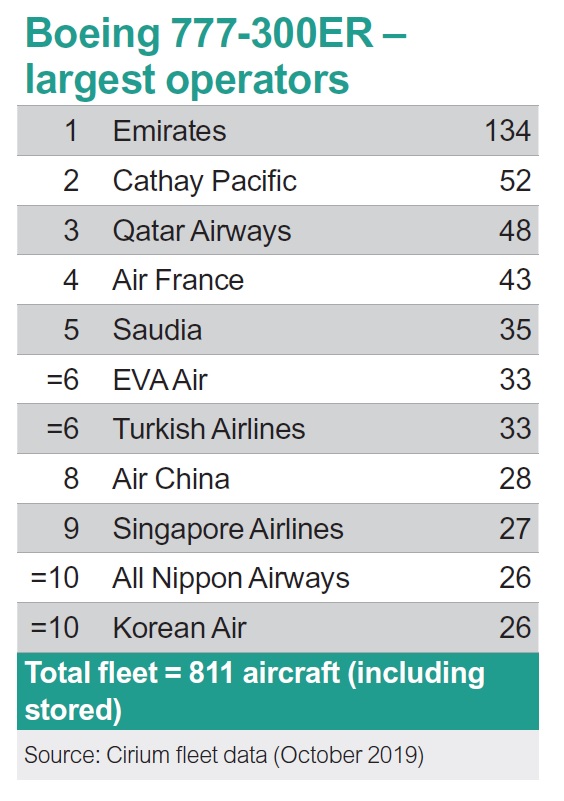

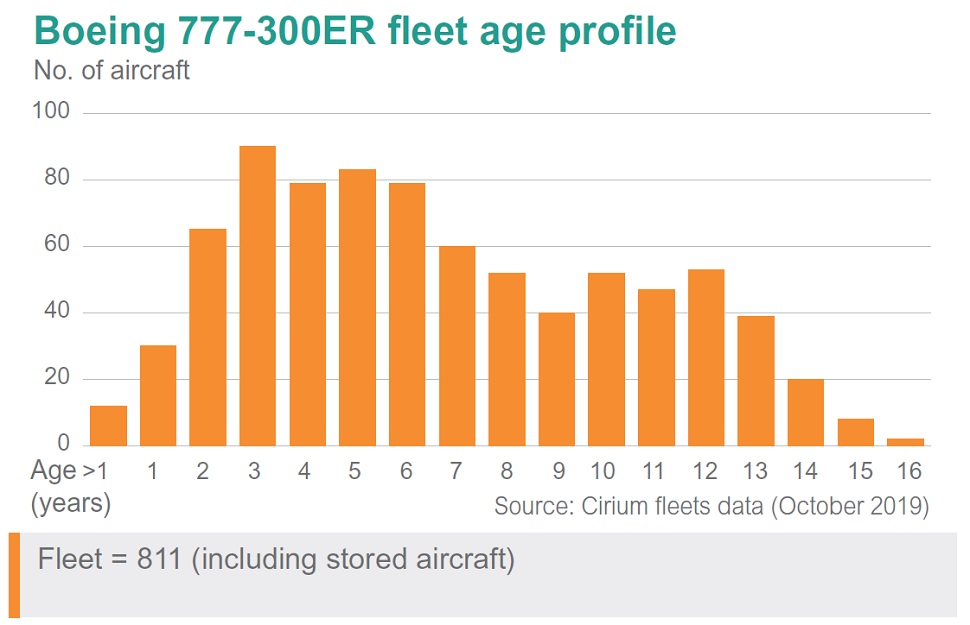

Cirium fleets data shows that there are 811 777-300ERs in service or temporary storage, with a further 33 on firm backlog for delivery before production is due to end next year. By far the largest operator is Emirates, with 134 in service (see table above). The oldest aircraft are 16-17 years old, with the bulk of the fleet in the 4-8-year age range.

“Traditionally, you would convert aircraft at around 15-16 years, but we may look at doing it a little bit earlier – between 12 and 16 years,” says Greener. “And that’s mainly because the mission of this aircraft might be more international so will have high utilisation.”

Greener sees the -300ERSF launch as providing a vital secondary-market application for the type. “It’s a case of ‘build it and they will come’,” he says, with the main target markets being e-commerce and express operators. The list price for the conversion has not been disclosed, but it is understood to be in the range of $35 million.

GECAS forecasts an overall market for 350 new and used widebody freighters through to 2030. Of these, GECAS believes the -300ERSF can capture 40-50% of the overall market (up to 175 aircraft), with the remainder being taken by new-build freighters.

Rob Morris, who is global head of consultancy at Ascend by Cirium, welcomes the arrival of an after-market conversion for the 777-300ER as it will provide an important future market option for ex-passenger aircraft. The 2019 Cirium Fleet Forecast predicts 70 777-300ER cargo conversions from 2024.

“We expect there will be a significant number of 777-300ERs showing up in the secondary market – we estimate as many as 120 lease expiries through 2024. Many of these are with operators who have already identified the 777-9 or Airbus A350 as replacements, and thus the returns are likely to go ahead,” he says.

“777-300ER passenger transitions so far have been relatively rare – there are only just over 20 now operating with an operator subsequent to the original one,” Morris says, pointing out that with the -300ER still being relatively young, this is not necessarily unusual at this stage.

“However, the majority of these transitions have been to operators in Russia,” Morris says. “One wonders how many more aircraft of this size that market could need. So placing these returns in the secondary market will be a challenge.”

The market values and maintenance status of target airframes for conversion will be a crucial part of the equation, Morris says.

“Our current estimate for the part-out value of a -300ER in half-life condition is between $35.7 million and $52.6 million. We suspect that some will head that way and thus, as aircraft start to be parted out then the lower estimate declines to around $25 million by the middle of the next decade. At this value, attractive freighter-conversion feedstock could be available.

“But then the cost of the conversion and associated maintenance will be pivotal. If the selected conversion airframe requires significant maintenance – for example, shop visits for the GE90-115B can be up to $15 million each – that will be a challenge. So minimising the cost of conversion will be key to broadening the market appeal and maximising conversions.”